Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

December 1, 2025

The investor romance with technology stocks (and those focused on artificial intelligence in particular) hit some of the largest setbacks in November since the ‘Deepseek scare’ earlier this year. These worries surfaced even though industry leader and ‘poster child’ for the AI boom, NVidia released their third quarter earnings report. They once again blew past expectations, raised guidance for the next quarter and continued to talk about a robust backlog and ongoing strong demand from all their customers for the next few years at least as they scale up data centres and AI applications. The company maintains better than 90% market share for GPUs with strong gross margins of over 70%. Stocks opened up strongly the next day and then did a major downside reversal around midday, giving up all the early gains and finishing sharply lower. The technical picture was also very disturbing on that 200-point reversal on the S&P500, with decliners leading advancers by a 3 to 1 ratio and new lows on the NYSE also tripling the number of new highs. While the S&P500 did manage to recoup those losses and finish flat on the month, the ‘technology heavy’ Nasdaq Index had a rougher time, dropping almost 2%. The more interesting stories, though, were not in the indices but in the individual large cap stocks. Nvidia had its worst month this year, falling over 12% despite the earnings beat. Other big ‘chip’ names were also down, with industry stalwart AMD losing almost 20%. Amazon and Microsoft were also under pressure, with each dropping 5%, while some former highflyers got their wings clipped, with Palantir giving up over 20% on the month and Coreweave dropping almost 50%. The biggest ‘canary in the coal mine’ though was Oracle. Larry Ellison’s data base software giant had surged over 30% in September on news that it would be receiving orders from OpenAI that would lead to over $300 billion in sales over the next five years. Further investigation into the real sustainability of that spending as well as the ‘creative’ financing proposed to pay for it caused Oracle to give back all those gains and then some in the past two months, dropping almost 40% from that October peak. The partial offset to all of this was Alphabet, which rose over 12% on the month as they got rave reviews on their newest version of their AI model, Gemini, which offset much of the worry that their core search business (Google) was going to be marginalized as AI usage increased. The model includes new tools such as Deep Think, for projects that require more stringent reasoning; generative user interfaces; and improved “vibe coding” for software developers, among other benefits. Gemini has been closing the gap with ChatGPT, with 650 million monthly active users to ChatGPT’s 800 million weekly active users.

It is now looking more like a tug-of-war going into year-end on the stock market between opposing themes. On the bullish side we have strong momentum and optimism about further interest rate cuts from central banks. Nvidia numbers and outlook provided relief over investor worries about the outlook for AI spending while strong numbers from Walmart relieved some investor worries about the strength of the consumer following the more guarded numbers and outlook from Home Depot. Tax related reasons have also been a factor as aggressive year end tax loss selling should start to abate. Strong markets this year have put many taxable investors in positions where they were pushing harder on losers to offset strong realized capital gains. As that selling slows down and they don’t want to take any further gains in the current tax year, we might see a bit of a ‘buying vacuum’ going into year end that could allow stocks to rally further. Also, insider buying has returned as executives at publicly listed companies bought shares in their own firms over the past 30 days at the fastest clip since May, stepping in as fears of an AI-bubble sparked a broad rotation out of highly valued tech stocks into more defensive pockets. As a result, the ratio of insiders buying to selling is up to 0.5.

The more worrisome issues for investors are the facts that gains have already been strong for the year, valuations are extremely stretched, and sentiment is unequivocally bullish. The breakdown in the crypto market, with Bitcoin at one point dropping more than 30% from its October peak, is another sign that investors have moved into a ‘risk off’ mode. Meanwhile the lack of any further major data points before the Dec. 9-10th Federal Reserve meeting suggests that the more hawkish rhetoric coming from a majority of Fed votes will stop them from cutting interest rates again this year. Tech stocks had already run into a small wall of selling in November as two of the biggest tailwinds for the sector in the past two years ran into some resistance, those being the growth of negative free cash flows for some of the major players and some questions about whether the depreciation schedules for AI chips were too long and therefore overstating actual earnings. Another headwind for stocks in the past month had been a more hawkish tone coming from some regional heads of the districts of the U.S. Federal Reserve, which temporarily reduced the odds of another interest rate cut at their December meeting. The rate-cut sceptics had argued that a slowdown in jobs growth may reflect changes in immigration policy and technology, rather than a serious deterioration in demand for workers that threatens a sharp rise in unemployment. They also noted that inflation has run above-target for several years, undermining the Fed’s credibility if they once again embark on a new easing regime while inflation remains elevated. The probability of another cut in December had been running at close to 100%, then dropped to under 40% when the hawkish regional Fed governor comments came out before rising again to over 60% New York Fed Chair John Williams re-iterated the more dovish views. Bottom line is that the December decision still seems like a coin toss but, more importantly, may be more indicative of the kind of divisions we start to see in 2026 when President Trump appoints a new head of the Federal Reserve and tries to fill more of the seats at that table with members that share his desire to see lower interest rates. For now, we believe next month’s decision may be a “hawkish cut” – a small reduction in interest rates accompanied by a statement that no more are planned. A final worry is that investor sentiment and positioning are at bullish extremes, which also increases the risks to the downside. The latest Bank of American investors survey showed that global investors lifted equity and commodity allocations in November, but cash holdings fell to just 3.7 per cent, triggering BoA’s “sell signal” and raising concerns that bullish positioning could act as a headwind for risk assets.

The bigger factor for stock prices in 2026 will be whether the elevated spending on AI infrastructure can continue at these rates, especially if there are no measurable returns yet from those investments. That worry seems to have shown up more sharply in the past month. In terms of free cash flow, the massive spending on AI infrastructure has used all the available cash flow from the major hyperscalers and sent them to the bond market to find funding. There is a growing belief that depreciation of the AI buildup is being understated since the useful life of the semiconductors and other infrastructure is shorter than the depreciation being applied, meaning that technology earnings are being over-stated. Credit default swap spreads on Oracle and CoreWeave debt have surged in recent weeks, reflecting growing scepticism surrounding the sustainability of current infrastructure spending. Oracle has seen consensus free cash flow estimates turn negative, with a significant portion of future revenue tied to OpenAI, which seems to be at the centre of most of the questions about valuations in the sector since it is still a private company. From the data we see, it doesn’t have the income to cover its costs. It expects revenue of $13 billion this year to more than double to $30 billion next year, then to double again in 2027, according to figures provided to shareholders. But costs are expected to rise even faster, and losses are predicted to roughly triple to more than $40 billion by 2027. Things don’t come back into balance even in OpenAI’s own forecasts until total computing costs finally level off in 2029, allowing it to scrape into profit in 2030. Meanwhile, investors keep increasing the valuation as new money goes in, with the latest round valuing this company at over US$500 billion! As for infrastructure stocks that are building data centres, they’ll need to transform their massive investments into real returns. Bain & Co. estimates that to justify their cost, these data centres will need to generate $2 trillion in annual revenue by 2030. With current revenues of roughly $20 billion, the business would have to expand a hundredfold.

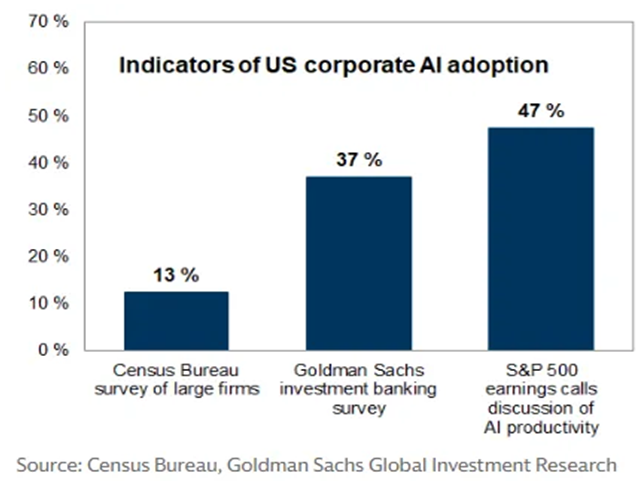

Once again, to justify these unheard-of levels of spending, the builders will need to see massive adoption of AI as well as associated payments and fees. Trying to quantify that number and assess the chances that the targets are reached are even more difficult. The definitions that companies use are varied. These are the percentages that have adopted AI, according to the Census Bureau and to Goldman’s own survey of companies, along with those claiming on earnings calls to be using it. The chart below shows how varied these responses are and why markets will continue to be volatile as the true usage and return on investment could take a long time to fully realize.

The parallels to past technology buildouts are hard to ignore. In the late 1990s, telecoms, such as Global Crossing and AT&T, spent over $500 billion laying fibre-optic cable in anticipation of rapid internet adoption. However, their projections proved over-optimistic, leaving the industry to suffer for years amid a glut of capacity and collapsing prices. The stakes are even higher this time around since the spending levels are that much higher, as are the return expectations!

Bitcoin, the poster child for the risk-on trade, collapsed more than 30% from its high before recovering a bit into month end, while gold has held its value above $4,000 per ounce. The Bitcoin-to-gold ratio has corrected down to a 14-month low. The Bitcoin-to-gold ratio and the S&P 500 are 88% correlated with each other! Several factors have driven the recent plunge in crypto prices. First, investors now are unsure if the Federal Reserve will cut interest rates again in December. If the central bank holds borrowing costs steady, that will make Bitcoin and its peers less appealing relative to interest-bearing investments such as bonds and savings accounts. Second, the market has decided this is a good time to rotate out of risk assets, amid questions about lofty artificial-intelligence valuations. A third issue is that many investors bought Bitcoin at around $90,000. With it now trading below that, they may be hesitant to keep buying while their investments are underwater, especially if they borrowed money to buy it and are now facing margin calls. That is when brokers demand more cash from investors to cover the loans. That, in turn, can lead to forced selling, which puts additional negative pressure on the asset’s price. Retail investors have for years been reliable buyers of pullbacks in American equities. However, there have been signs resilience is being strained. One is in crypto, where shockwaves extended the over-$1 trillion total market value loss of all cryptocurrencies. In the stock market, exchange-traded funds have been among the month’s biggest losers. Twelve of 16 are showing double-digit losses in November, including three leveraged funds that are down more than 40%. The crypto crash isn’t just hurting Bitcoin bulls. Investors in top brokerages like Robinhood, Coinbase and Interactive Brokers, which have been some of the market’s hottest stocks this year, are getting clobbered as well.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.