Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 4, 2025

The Canadian bond market narrowly avoided suffering its third consecutive monthly decline in May as higher than expected inflation and a weak U.S. bond market caused Canadian bond yields to rise and prices to decline. Interest earned was just sufficient, though, to offset the lower prices. U.S. President Trump continued his pattern of applying massive tariffs but then postponing their implementation. Of particular importance in May was an agreement between the U.S. and China to reduce most of their respective tariffs for 90 days, which led to optimism that a resolution of the potential trade war could be found. The potential improvement in the economic outlook caused a strong rally in equities and helped corporate bond yield spreads to narrow significantly. Trump also threatened the European Union with 50% tariffs but subsequently postponed their implementation to allow negotiations. The FTSE Canada Universe index returned +0.02% in the month.

Likely the most impactful Canadian economic data received in May was that concerning inflation. The removal of the consumer carbon tax in April caused the headline rate of CPI to fall to 1.7% from 2.3%. However, excluding energy, the pace of inflation accelerated. The core rates of inflation, of note, rose to 3.15% from 2.85% the previous month, which led bond yields to jump higher as expectations of additional rate cuts by the Bank of Canada were pushed further into the future. Other economic data received in the month were mixed. The unemployment rate rose to 6.9% from 6.7%, in part because of a rise in the participation rate, but also because job creation stalled with the tariff uncertainty. More positively, both housing starts and retail sales were better than expected. On the last business day of the month, we learned Canadian GDP grew at a better than expected pace of 2.2%. However, the strength was due to a surge in exports and inventories ahead of the threatened U.S. tariffs. The uncertain environment has stalled domestic economic growth, which was reflected in GDP for the month of March increasing only 0.1%, and advance data suggested a similar increase in April.

In the United States, a discrepancy has developed between so-called “soft” data that measures opinions and sentiment and “hard” data that reflects actual activity. The soft data has suggested that Trump’s tariffs will cause a marked slowing of the U.S. economy and significant inflation. For example, consumer sentiment dropped near its all-time lowest level while expectations for inflation over the next year surged to 7.3%. Hard data, though, did not corroborate the soft data. The unemployment rate remained at the low rate of 4.2% and CPI inflation edged lower to 2.3%. The U.S. Federal Reserve left its interest rates unchanged at its May meeting, as it waited for more evidence of the impact of Trump’s tariffs.

The U.S. House of Representatives narrowly passed a massive budgetary bill that sought to implement President Trump’s many policies and initiatives. Unfortunately, the bill’s proposed tax cuts were larger than its anticipated spending reductions, meaning the U.S. fiscal deficit would increase to more than 7% of GDP for the next decade. The prospect of substantial increases in the supply of U.S. Treasuries to fund those deficits caused their yields to move sharply higher. The yield of 30-year Treasuries briefly went above 5.00% for only the second time since 2007. The bill now moves to the U.S. Senate for its consideration, but there is little expectation that the deficits will be meaningfully reduced.

Also in May, Moody’s lowered the United States’ sovereign debt rating from Aaa to Aa1, citing the $36.2 trillion accumulated debt, rising net interest costs, looming tax cuts, and political gridlock. Moody’s downgrade aligned its rating with those of Standard & Poors and Fitch Ratings which had downgraded the U.S. in 2011 and 2023, respectively. The Moody’s downgrade announcement had limited immediate impact in the bond market but may have longer term implications if it discourages conservative investors from purchasing Treasuries in the future.

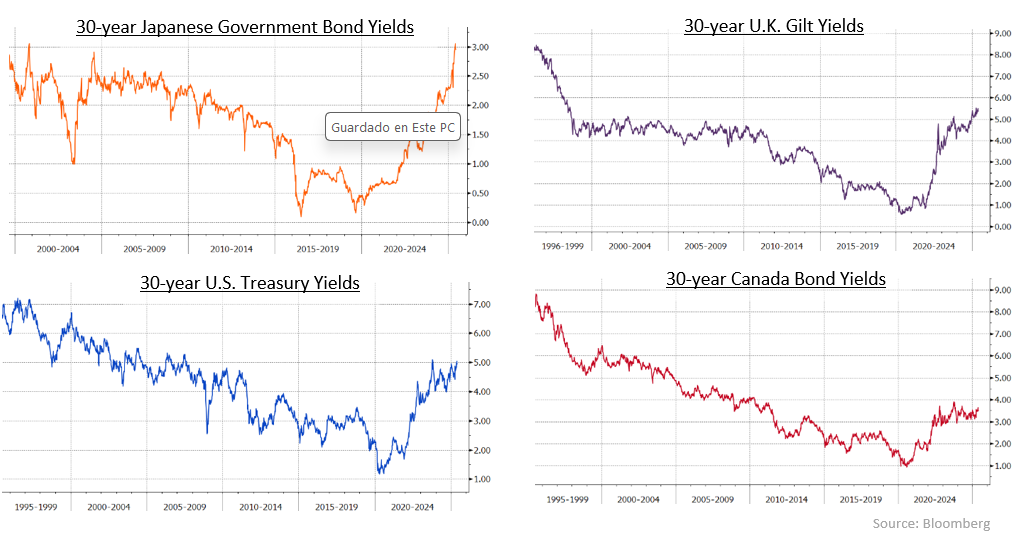

Internationally, the rise in 30-year U.S. Treasury yields occurred as other countries’ bond yields were also moving sharply higher. For example, the yield of 30-year Japanese Government Bonds hit their highest level since their initial issuance in 1999. The Bank of Japan announced plans to reduce its purchases of new JGBs, which led to a weak auction of 20-year JGBs and a selloff in other long term maturities. A higher than expected Japanese CPI release also led to higher JGB yields. Should those higher yields persist, they may encourage long term Japanese investors, such as life insurance companies, to switch from buying U.S. bonds to purchasing domestic issues instead. In Britain, yields of 30-year Gilts rose to their highest level since 1998 following a large jump in the inflation rate.

The rise in Gilt yields came despite the Bank of England lowering its interest rates by 25 basis points. In contrast with other bond markets, Canadian long term yields were not close to their record levels. Elsewhere, the Reserve Banks of Australia and New Zealand also lowered their respective interest rates by 25 basis points.

Canada bond yields of all terms rose in May. The yields of 2, 5, and 10-year bonds finished roughly a dozen basis points higher, while 30-year yields gained a more muted 6 basis points in the month. In the United States, concerns about the fiscal deficit caused much larger increases in Treasury yields. The yields of 2-year Treasuries jumped 29 basis points higher, while 30-year Treasury yields rose 25 basis points.

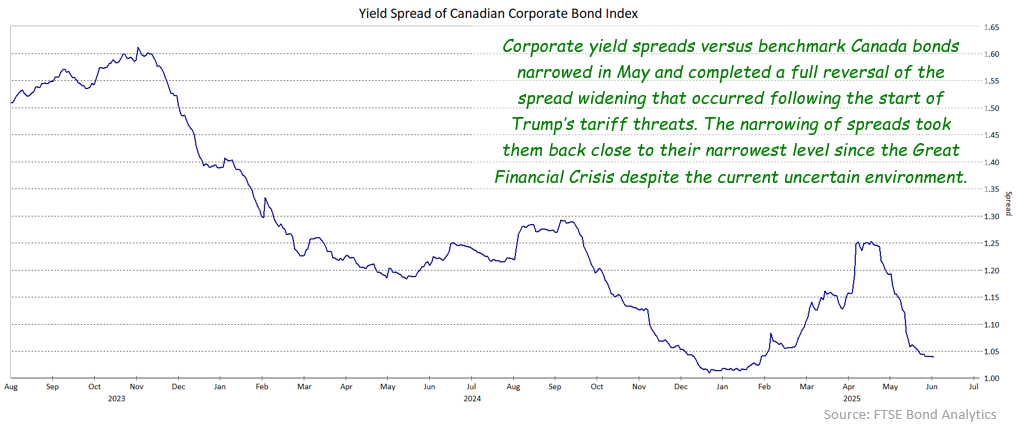

The federal sector declined 0.36% in May, as the lower yields of Canada bonds failed to offset the impact of the increases in yields on bond prices. The provincial sector returned +0.09% in the period, helped by their yield spreads narrowing an average of 4 basis points in the risk-on environment. The corporate sector benefitted from robust investor demand and earned +0.58%. Notwithstanding the uncertain economic environment, the risk premiums of corporate bonds, otherwise known as yield spreads, compressed an average 13 basis points in the month. In doing so, corporate yield spreads have reversed all the widening that occurred after Trump began his tariff trade war. Non-investment grade corporate bonds also

benefitted in the risk-on environment, gaining 1.36% on average in May. The higher than expected inflation data spurred demand for Real Return Bonds, which earned +0.23% in the period and outperformed nominal Canada bonds of similarly long durations. The strongest performance in May came from preferred shares which rebounded strongly from their weak performance in April, gaining 5.05% in the month.

In the very short term, we expect bond prices will strengthen in early June due to changes in index durations. As a result of coupon payments and bonds with less than one year to maturity falling out of the index, the FTSE Canada Universe duration will increase 0.105 years on June 2nd. The long term index, which is sometimes used by pension funds, will increase by a record 0.665 years the same day as a very large quantity of 10-year bonds are removed from that index. In the past, index extensions such as these have led to significant purchases of long term bonds and we expect this will be repeated this time around. In addition, equity markets enjoyed much stronger returns than bonds in May, which may lead to additional bond buying if funds rebalance their asset mix.

The Bank of Canada is scheduled to announce its next decision on interest rates on June 4th. We expect the Bank will leave rates unchanged as the recent GDP data did not show sufficient weakness to require immediate monetary stimulus. In addition, the unexpected rise in inflationary pressure will probably make the Bank more cautious about lowering rates. While we do not see any likelihood that the Bank will raise interest rates over the balance of this year, the uncertain outcome of Trump’s threaten-and-postpone tariff antics mean future rate cuts are not a foregone conclusion, however. Over the next few months, we anticipate the uncertainty will continue to dampen economic activity in Canada, so we are comfortable maintaining somewhat longer than benchmark portfolio durations. We also believe that the recent tightening in corporate yield spreads means that they are not providing appropriate returns for the level of economic and financial risk. Accordingly, we are cautious about the corporate sector.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.