Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

January 23, 2025

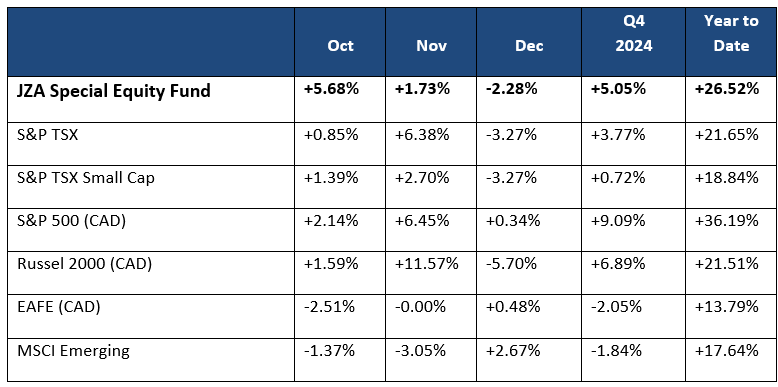

Welcome to 2025! I hope this year brings health, happiness, and prosperity to all. Equity markets delivered strong returns in 2024, with the S&P/TSX Composite Index gaining +21.7% and the S&P/TSX Small Cap Index rising +18.8%. While Canadian markets performed well compared to many international markets, they lagged U.S. large-cap indices, which were propelled by the outperformance of mega-cap stocks. Despite concerns about volatility, the small-cap fund excelled, delivering an impressive +26.5% return in 2024, significantly outperforming both Canadian and U.S. small-cap markets.

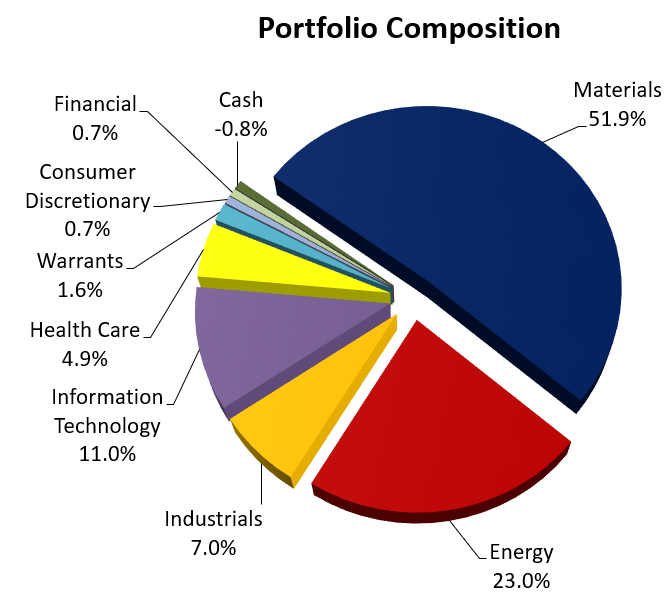

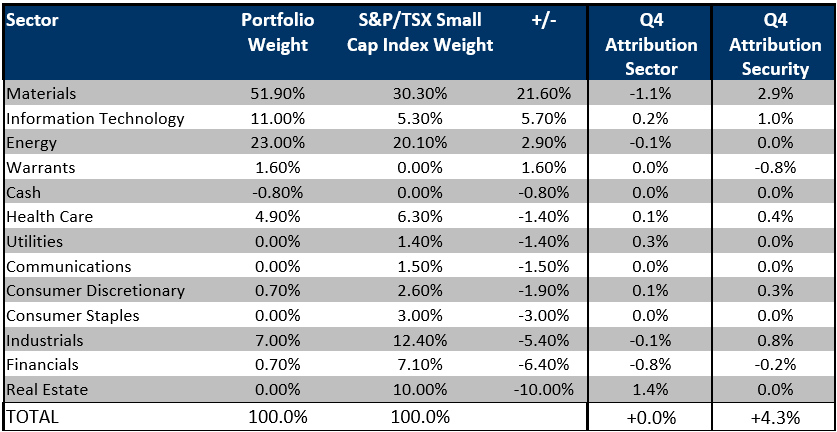

Stock selection contributed meaningfully to the portfolio’s overall outperformance during the quarter contributing all +4.3% of outperformance. Below are the portfolio components and attribution for the quarter.

In the fourth quarter of 2024, the portfolio’s performance was influenced by several key holdings. The three most significant detractors were Freegold Ventures, Rua Gold Inc., and Colabor Group, collectively reducing the portfolio’s return by -1.6%.

Freegold Ventures, which we have held for some time, is advancing one of North America’s largest undeveloped gold resources at its Golden Summit project near Fairbanks, Alaska. In September 2024, the company announced an updated mineral resource estimate, reporting 12.1 million ounces of indicated gold at 1.08 g/t and 10.3 million ounces of inferred gold at 1.04 g/t. Despite this positive development, the stock underperformed in Q4. We actively manage this position and had sold shares following the resource announcement. We continue to hold a core position, confident in the company’s management and the project’s potential.

Rua Gold Inc., a small-cap emerging gold explorer in New Zealand, holds two highly prospective land packages. The company has made significant progress, including intersecting visible gold and confirming downhole continuity of high-grade mineralization at the Murray Creek project in November 2024. Despite these advancements, the stock has underperformed recently as investors from the merged company used the liquidity to exit their positions. We anticipate increased interest as drilling and news releases continue and maintain our position accordingly.

Colabor Group, a leading distributor of food and related products, operates two warehouses/distribution centers in Quebec, supplying 10,000 products to 5,000 businesses. Established in 1962, the company has significant market share east of Quebec City and aims to replicate this success in the Montreal area by increasing capacity utilization at new plants. However, economic slowdown has delayed this expansion, contributing to the stock’s underperformance. We continue to hold our position, looking for opportunities to add when market conditions improve.

Conversely, the top contributors to performance in Q4 2024 were Aldebaran Resources, Founders Metals, and MDA Space Limited, collectively adding +2.8% to the portfolio’s return.

Aldebaran Resources is advancing the Altar copper-gold project in San Juan, Argentina, one of the largest undeveloped copper assets held by a junior company. The project is part of a cluster of world-class porphyry copper deposits, including Los Pelambres (Antofagasta), El Pachon (Glencore), and Los Azules (McEwen Mining). Given the stock’s strong performance, we have reduced our position to manage its weight within the portfolio but continue to hold a core stake.

Founders Metals, a Canadian-based exploration company, is focused on the Antino Gold project in Suriname, located in the Guiana Shield. Having previously experienced success in this region with Reunion Gold, and noting that this property was once owned by them, we were interested in the opportunity. Impressed by CEO Colin Padget and the project’s potential, we have trimmed our position to manage portfolio weight but remain satisfied holders.

MDA Space Limited, founded in 1969, is a leading provider of advanced space technologies serving nearly all sectors of the rapidly growing space economy. The company has garnered significant attention over the past two years, resulting in above-average growth rates. We continue to hold our position but have trimmed it into strength.

Outlook for 2025

As we move into 2025, the economic environment is marked by heightened uncertainty and the potential for significant market volatility. The ongoing tension between rate cuts to stimulate the economy and the persistence of inflation remains a central theme. Treasury yields climbed sharply in the fourth quarter, with the 10-year yield rising to 4.76%, reflecting strong job growth, increasing consumer inflation expectations, and rising oil prices driven by geopolitical concerns. While markets had initially anticipated multiple rate cuts in 2024, the current outlook suggests only a modest reduction in 2025, adding to the challenges faced by investors.

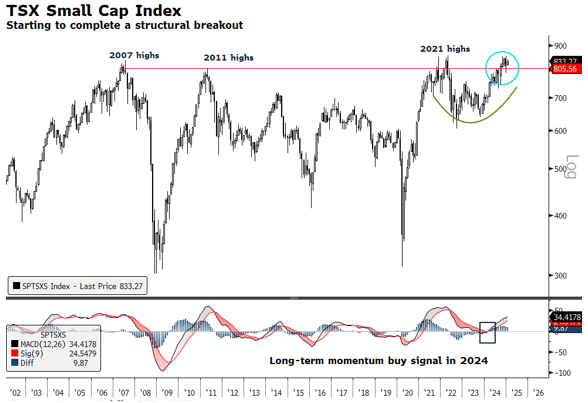

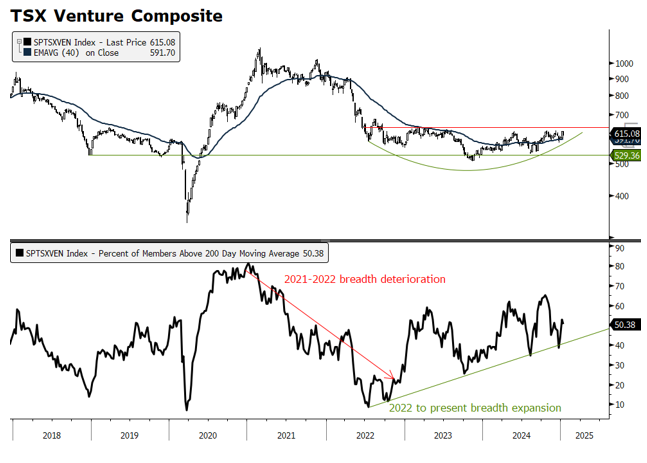

The charts below highlight the recent technical strength in the TSX Small Cap Index and the TSX Venture Index, underscoring the resilience of Canadian small-cap equities despite broader market volatility. Both indices have exhibited positive momentum, reflecting increased investor confidence in this segment of the market. The sustained upward trend in these indices provides a supportive backdrop for our positive outlook on Canadian small-cap equities in 2025.

The precious metals sector remains an area of confidence, driven by political uncertainty and sustained central bank buying. Gold prices, while influenced by currency fluctuations, are expected to benefit from heightened geopolitical risks and potential growth scares later in the year. The continued appeal of gold is bolstered by its role as a safe-haven asset, particularly as inflationary pressures persist.

Copper remains a compelling opportunity, particularly as larger companies in the sector seek production growth through mergers and acquisitions with junior miners. The sector continues to face tight supply conditions following years of underinvestment, and demand remains strong due to its critical role in electrification and renewable energy infrastructure. Last year, the sector lagged due to global economic weakness, particularly in Europe, China, and other emerging markets. However, these challenges have created attractive valuations, positioning the sector for long-term growth.

The energy sector has also seen a shift in our portfolio positioning, moving from an underweight to a slight overweight early in 2025. This reflects an improved outlook for natural gas, with LNG exports gaining momentum in Canada, and stronger fundamentals in the oil market, supported by the potential for U.S. sanctions on foreign crude supplies. Much of this increased weighting comes from service stocks, which are demonstrating more robust growth than many exploration and production peers. Additionally, the continued weakness in the Canadian dollar is enhancing profitability for domestic producers, further supporting our thesis in this sector.

The technology sector remains dynamic, following a year marked by small-cap takeovers and strong M&A activity. This trend is expected to continue, with larger firms seeking innovative smaller players to enhance their competitive edge. We remain focused on key holdings such as Illumin, Well Health, Tantalus, Kneat, Real Matters, and Tecsys, all of which demonstrate strong growth potential in their respective industries. The rapid evolution of technology in digital infrastructure and healthcare underscores the importance of maintaining exposure to this high-growth area.

Political uncertainty also adds complexity to the outlook for 2025, with the new U.S. administration set to introduce tariffs that could affect global trade and inflationary pressures. This backdrop further underscores the importance of remaining nimble and responsive to policy changes, currency fluctuations, and shifting economic dynamics. While headwinds remain, the opportunities in small-cap Canadian equities are encouraging, particularly in sectors like technology, copper, energy, and precious metals.

The year ahead will require vigilance and adaptability as we navigate these challenges. Despite the complexities, we remain optimistic about the renewed cycle of growth for Canadian small-cap equities, supported by strategic sector positioning and active management. Here’s to a successful and prosperous 2025!

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.