Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

January 3, 2025

The 2016 post-election playbook has worked so far in 2024, but we believe that 2025 may end up looking more like 2018 than 2017. When the 2016 election results were first known, stock futures took a major drop as investors had not expected the win, and the candidate seemed to have a lot of controversial policy ideas and was viewed as too volatile for market stability. However, the focus quickly turned to the benefits of major fiscal spending on capital projects, loosened regulations on financial services, a surge in oil drilling activity, tariffs to protect U.S. manufacturers and, to top it all off, the Trump Tax Cuts, which gave a huge boost to earnings growth. This all lead the stock market to have a huge year in 2017 without any significant corrections. However, by the end of that year the euphoria began to wear off and was replaced by some of the less bullish impacts of the new administration’s policies, including counter-vailing duties from their largest trading partners, pushback in congress from some of the spending initiatives and, most importantly, a move by the Federal Reserve (under new ‘Trump-appointed’ Chairman Jerome Powell) to start to increase interest rates to offset the potential inflationary impacts of the increased economic activity and surge in the budget deficit. The result was two significant stock market drawdowns in 2018 (10% in the first quarter and a ‘near 20%’ drop in the fourth quarter) resulting in negative returns for that year. We see similar risks going into 2025. The expected good news has been quickly and fully incorporated into earnings growth and stock valuations. Meanwhile, inflation has become ‘sticky’ in the 3% range, particularly for core services, which have remained resilient largely to the wealth effect. The imposition of duties and mass deportation of illegal immigrants will slow job growth but could also be inflationary. The spending initiatives and extension of the 2017 tax cuts will also increase the budget deficit further, putting more upward pressure on interest rates. We expect the Federal Reserve to be less willing to cut interest rates much further next year until they see a resumption of downward pressures on inflation. We expect only two more interest rate cuts of ¼ point each in 2025. That will be another headwind for stock valuations, which had been anticipating a much more aggressive downward path for rates.

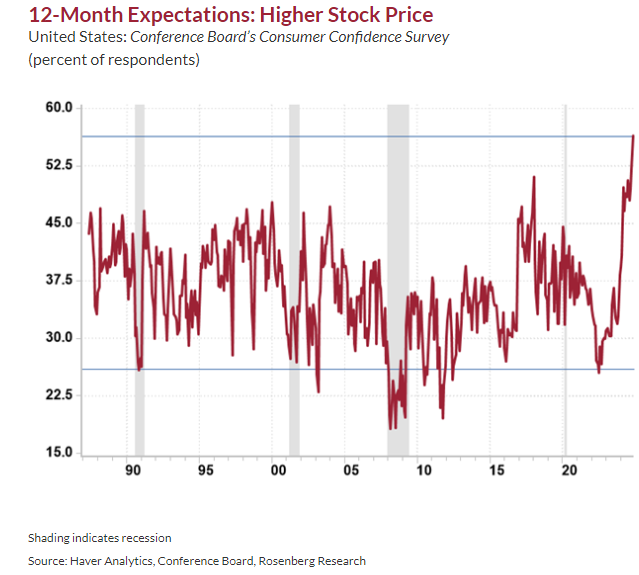

Stock market sentiment is ‘off the charts’ bullish. Market Vane is at a 73% bullish reading, the very high end of the historical range and right where it was in the summer of 2007. The Conference Board survey also shows household ebullience over equities has never been as high as is the case today. The UMich survey showed that in November, the median household owned a record $257,064 of stocks, a 75% boom over the past year. Households have a record 70%+ concentration of their financial asset mix in equities and at a time when the cash allocation level in Bank of America’s Global Fund Manager Survey is at its lowest since the survey began in 2001. There is no “dry powder” to be put to work. The Citi Panic/Euphoria index has moved up to 0.59 from 0.55 a week ago and has dramatically pierced the 0.41 threshold that defines euphoria. The Investors Intelligence survey shows the bull camp at 61.3% from 60% and the bear share is down to 17.7%. Well over three bulls for every bear and well above the extreme level reading of ‘net 40% bullish”. Moreover, the National Association of Active Investment Managers (NAAIM) “exposure index” is just below the highs of the year at 98.9. Meanwhile, equity portfolio managers are sitting at a historically depleted 1.4% cash-to-asset ratio. The chart below shows the Conference Board Survey which puts stock expectations for the year ahead at a record level. The bottom line on this bull market is that everyone is ALL IN!

The American Exceptionalism narrative has turned to gospel and culminated this year in the U.S. stock market capitalization expanding to an record level of 75% share of the world equity market. It was below 60% in both the other two made-in-America bubbles: the Nifty Fifty in the early 1970s and the tech mania of the late 1990s. Two of the most overused phrases we hear recently are ‘animal spirits’ and ‘American exceptionalism.’ We expect that next year at this time, those two phrases will be quoted far, far less! One final note, if you believe at all in the fallacy of ‘headlines risk’, then just take a quick look at the top story on the noted financial journal Barrons this past weekend: Stocks Could Gain Another 20% in 2025. Embrace the Bubble.

Investors have become so enamoured with the potential for gains from artificial intelligence that even the reference to potential gains from the implementation can save otherwise mediocre earnings reports. We saw that recently with tech darlings Palantir, Broadcomm and SalesForce, where expectations were basically met but in the ‘post earnings’ conference calls they all gave indications they would have growth in AI related products and the TAMs (Total Addressable Markets) for these products were higher than previously believed. All three stocks were already trading near record valuations going into the reports and only got more expensive following the reports. Expectations are rising and the risks are the lofty goals are not met! One final note on the mantra of ‘U.S. exceptionalism’. Despite all the society-changing innovations in recent decades, real US GDP growth has averaged just 2.1% annually since 2000, compared with 3.7% during the preceding half-century. Without accelerated population and labour force growth, even restoring the productivity growth of the pre-2000 period would boost real GDP growth by just 0.5% annually. While that 2.1% real growth rate over the past 25 years certainly exceeds what we’ve seen in Canada, Europe or Japan, it nonetheless represents the growth rate of a mature economy.

Given the dour outlook described above for the next year, we have a very defensive investment strategy going into 2025. We have an overweight position in cash, where returns are still close to 4%. We also have increased our position in U.S. long-term (20+ year) government bonds in the U.S., where the yield is around 4.7%. This position is also a good overall hedge for stock exposure in the portfolio since we expect that bonds would rally on either stock market or economic weakness, while still providing strong income. We also continue to hold gold stocks as a hedge against potential U.S. dollar weakness as well as due to their multi-decade low valuations relative to the price of gold. In stocks overall, we have a slight underweight asset allocation (around 45%) and within that allocation we tend to have a ‘barbell’ approach, with a mix of high dividend yield, low valuation, stable earnings sectors such as pipelines, energy and telecoms. At the other end of ‘the barbell’, we continue to hold positions in the growth sectors, particularly health care and technology. Biggest U.S. names include Pfizer and CVS in health care and Alphabet, META, Amazon, Shopify, UBER and Micron in technology. We are underweighting financials, consumer and industrial stocks due to excessive valuations and our perceived earnings risk. We have recently reduced our holdings in Canadian banks (BMO and BNS sold outright) due to valuations that are at the highest end of the historic range and ongoing economic risks, particularly from trade tariffs. However, we feel that most of the downside risk is already reflected in the price of TD Bank, and we have added that stock back into the portfolio.

“If You Build It They Will Come,” But Will AI Investments Deliver This “Field of Dreams”? Unlike the classic 1989 film, we are not referring to building a ballpark in a cornfield but to the unprecedented spending on the infrastructure needed to support the supposed demand for the plethora of artificial intelligence offerings that are supposed to change our lives and improve the productivity of businesses in a profound way. While we have many concerns about the outlook for stocks going into 2025, one of the longer-term issues that we also believe will be a headwind for stocks are the expectations that have been built into the technology stocks (and the rest of the market) for the implementation of artificial intelligence on a timely AND profitable basis. This is not necessarily a short-term risk since we know that the massive buildout of data centres and cloud businesses to accommodate the infrastructure needed to support the large language models that will be used for the implementation of artificial intelligence (AI) will be ongoing for now. The big hyper-scalers (Meta, Microsoft, Alphabet, Apple) are not spending millions or even billions on this build-out. They are spending ‘hundreds of billions’ each year! But that level of spend is also why we see the risk. At some point there will have to be a return on these investments, and we have yet to see either the specific software, productivity enhancements or consumer applications that will make this a ‘must have’ for all businesses and individuals. I started our company in the early 1990s and immediately saw the benefits of using the new Excel spreadsheets and the data loads to be able to dramatically decrease the time involved in managing investment portfolios while simultaneously increasing the information from those reports. Ditto for the rollout of smart phones a decade later and how they were able to accelerate the adoption of the social media platforms that have become integral parts of almost everyone’s life. Cloud computing a further decade later accelerated the movement to SAAS (software as a service) and lead to a decade of additional growth for all the companies that could roll out those offerings. The most classic example of that success was how cloud computing resurrected growth at Microsoft, which had stagnated as desktop computer sales moderated. The move to cloud-based services at Microsoft helped deliver a 10-fold increase in the stock price between 2013 and 2023.

For all those earlier technology breakthroughs there were associated profitable uses for business and individuals that were visible and immediate. But as we enter 2025, the scale of spending on AI infrastructure is multiple times what was spent on any prior technology rollout. That means the returns also need to be that much larger to justify this spending. We remain sceptical that the productivity enhancements and consumer applications will arrive in sufficient quantities to justify the amounts already spent to build this capacity as well as the valuations of those stocks.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.