Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

November 2, 2024

For all the worries about the impact of the U.S. election on markets, the path of interest rates from the U.S. Federal Reserve and the outlook for corporate profits going into the most volatile period of the year, stock markets ended up being relatively quiet in October. The stock market also had to fight against rising longer-term interest rates as sticky inflation reduced the bullishness about multiple interest rate cuts by the Federal Reserve. Meanwhile, continued massive fiscal deficits and the funding required to finance them did push bond prices lower. The U.S. government 10-year bond yield, which was 3.6% when the Fed made their surprise 50 basis point interest rate cut on Sept 16th, have surged to 4.27% since that day. Despite those headwinds, U.S. stock indices were mostly unchanged on the month as strength in financials offset weakness in energy and technology. It was a similar story in Canada although we ended with a slight gain on the month as the heavier index weight of the financials in Canada helped generate better relative results. Outside of North America there was weakness almost everywhere as the geo-political risks, dismal economic numbers and a lack of great stock stories such as the AI euphoria in the U.S. lead to negative returns in all the industrialized markets, except for Japan. European stocks were down 3.5% on the month while India was a notable weak spot in Asia, falling 5.8%.

Tech Earnings Review: With the final two big tech earnings reports of the week (Amazon and Apple) in the books we can clearly see that the tech/AI/cloud/data center spending binge is not easing up any time soon. But investors were not impressed enough by the plethora strong tech earnings reports as they focused more on the realization that the costs of this AI rollout will continue to be substantially more than expected. Meanwhile we have seen uninspiring earnings from most of the rest of the market. Shortfalls in big ‘economic bellwether’ names such as McDonalds, Stellantis, Ford, Coke, Starbucks and Caterpillar suggest to us that earnings growth estimates are still too high. We are looking at 4-5% year-over-year growth for the third quarter and yet we still see analysts pencilling in 12-15% earnings growth in 2024, at the same time as we are seeing economic growth lose momentum. While many investors had hoped for a continuation of the expansion of market breadth, the lack of strong earnings and outlooks outside of the tech sector means that the big tech stocks are not in the process of losing leadership. Valuations are certainly elevated in many cases in that group, but the results show that most of those valuations are ‘well earned.’ Of course, not all ships are rising, and investors need to be wary of the downside risks associated with high valuations and lofty expectations. Eli Lilly, Uber, AMD, eBay, Coinbase and SuperMicro Computer all showed us this week just what the reaction to disappointments can be. The bar is set very high in the sector, so companies need to deliver. Alphabet did just that with 25%+ growth in cloud computing, a major recovery in ad spending and a reduction of over 80% in search costs from the effective implementation of AI on its search engine. Meta also delivered good numbers that were in line with expectations, but investors did not like their increased capex. They want to see results from prior spending, not new initiatives. Their ad revenue growth also lagged that of Alphabet. Meanwhile, their ‘Reality Labs’ unit continued to show operating losses, and the uptake was less than expectations. Microsoft also beat the estimates on continued growth in its cloud services Azure division, which grew at over 30% year-over-year. But there was disappointment on expectations of slower cloud growth going forward, the lack of detail on the uptake of their ‘Copilot’ services and the fact that the valuation is basically at the top end of its recent range. Our holdings in the technology sector continue to be Shopify, Celestica and Lightspeed in Canada and Meta, Alphabet, Amazon, Micron and Nvidia in the U.S. We have, though, reduced weights in those semiconductor stocks recently.

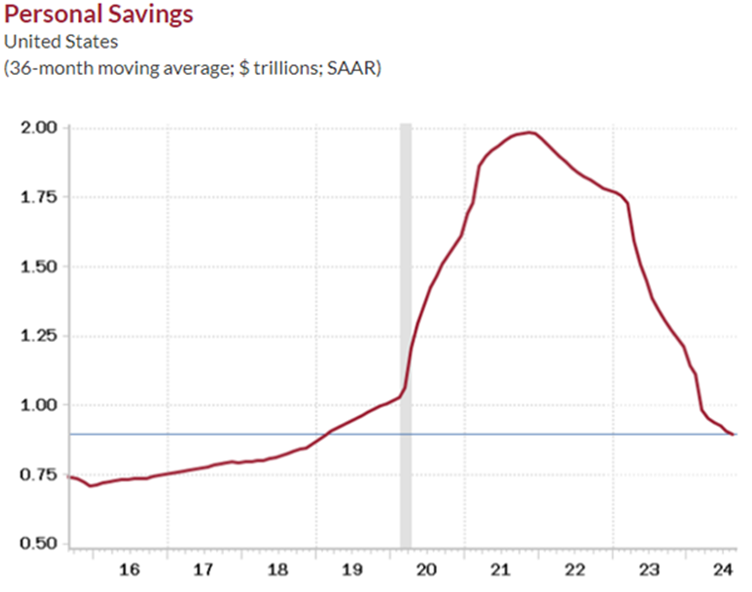

This has been the ‘mother of all’ momentum-driven stock markets. It certainly has not been about earnings. Third-quarter EPS growth is poised to advance +5% on a year-over-year basis while the S&P500 has soared over 40%. To continue rising, this market will need more solid economic and earnings support across the board. But we don’t see this happening as the pandemic-era excess savings have been fully unwound. This tailwind for the consumer since early 2021 is gone which is important since the ongoing decline in the savings rate has been promoting sustained gains in consumer spending. That, along with the ‘wealth effect’ impact from the massive gains in both stock prices and home values, have kept economic growth in the U.S. running at ‘artificially high’ levels. But, with the savings rate having declined from a peak of over 7% to the current level of about 2.5%, the pandemic era savings are now gone.

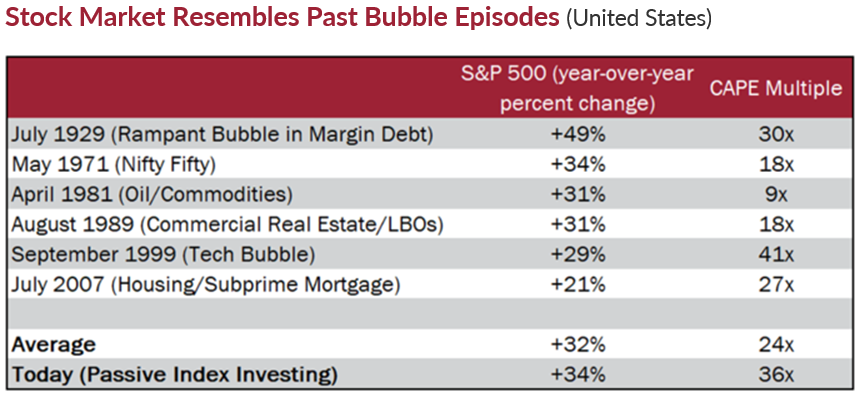

Sentiment has also gone ‘off the charts’ bullish in the past month, raising worries once again that investors are ‘all in’ and there might be more downside risks in the near term. The October Bank of America Global Fund Manager Survey, a monthly survey of global fund managers, was about as optimistic as you could get. Fully 90% expect a “soft landing,” or “no landing” at all (i.e. the economy remains strong). Corporate buybacks have also been a major factor in the rally this year. Goldman Sachs estimates U.S. corporations themselves are the largest buyer of the U.S. equities market in 2024. Goldman estimates $988 billion in announced buybacks were made so far in 2024, up 21% from 2023, which itself was a record year. The American Association of Individual Investors sentiment survey shows bullishness near the highest levels all year. Bullish sentiment at 49% is very high: the historic average is 37.5%. The table below illustrates all the other times when the S&P500 was approaching a peak with returns on a year-over-year basis remotely close to where it stands today. The CAPE Ratio (also known as the Shiller P/E or PE 10 Ratio) is an acronym for the Cyclically-Adjusted Price-to-Earnings Ratio. The ratio is calculated by dividing a company’s stock price by the average of the company’s earnings for the last ten years, adjusted for inflation. So it is really a ‘long term valuation’ tool. Its current read of 36 is more than 50% above the long-term average value and is surpassed only during the ‘tech bubble’ of 1999.

Stock investors could hardly be more enthusiastic: The S&P500 has raced higher, notching its best first nine months of a year since 1997. U.S. households’ equity allocation as a share of total financial asset holdings has never been higher at almost 45%, according to JP Morgan. Yet some of the best-informed investors don’t seem to share the optimism. Corporate insiders have been reluctant to snap up shares of their companies. Of all U.S. companies with a transaction by an officer or director in July, only 15.7% reported net buying of company shares, according to InsiderSentiment.com. That was the lowest level in the past 10 years. During the pandemic-induced selloff of early 2020, insiders raced to scoop up shares, buying nearly $1.3 billion in March alone. Some investors took it as a reassuring sign. This year, the largest insider trades have been sales by leaders of big tech companies. I also find it very interesting that we pointed out above that corporate buybacks are at record highs, but insider buying is near 10-year lows. It tells me that CEOs and other directors are happy to use the ‘company’s dime’ to buy back stock and keep valuations high but are less enthusiastic about putting their own money behind those purchases.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.