Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

September 5, 2024

It began badly. But four weeks on from the worst volatility blowup since the pandemic, August will just go down for now as another opportunity to ‘buy the dip’ in the stock market. After all the early month volatility and ‘near panic’ about emergency Federal Reserve interest rate cuts, the S&P 500 posted a 2.3% gain as it notched its fourth straight winning month. A surge in consumer staples, real estate and health care helped lift the broad market index in August. In Canada, the TSX Composite Index also sold off early in the month but came back to post a 1% monthly gain, lead by solid gains in the telecom, information technology, real estate and financial sectors, following reporting from the major banks that mostly beat the tepid expectations. The month had gotten off to a rocky start, though, as the major averages suffered a steep sell-off in the first week, with the S&P500 losing as much as 7.3% before recovering, while the ‘technology heavy’ Nasdaq Index was down as much as 10.7% as the artificial intelligence stock trade was ripe for some profit taking and the implosion of the crowded ‘Yen Carry Trade’ lead to a 12% one-day sell-off in the Nikkei Index in Japan. But cooler heads ultimately prevailed and, for now, at least, nothing in economic data or corporate earnings is screaming imminent danger, only an ongoing weakening. Yet if there is a lesson in August’s rout, it’s that consensus bets such as going long artificial intelligence or exploiting the weakening yen, can backfire suddenly. That is particularly noteworthy as we head into September, statistically the worse month of the year for stocks.

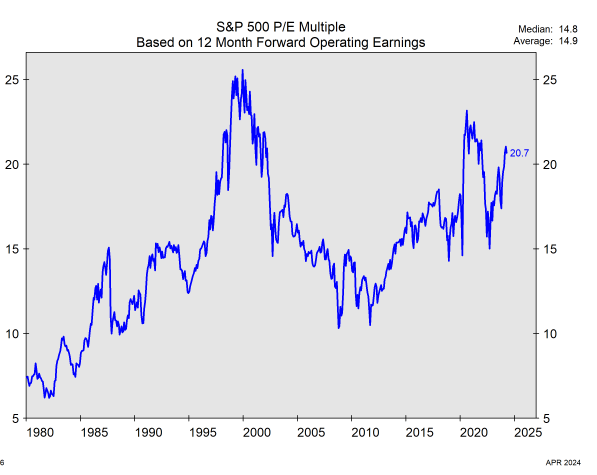

The August sell-off was probably more pronounced and rapid due to the aggressive positioning and sentiment of investors going into this month, as investor sentiment had been very extended, and investors were ‘all in’ on the trade in stocks. The Market Vane weekly Bullish consensus had risen to 72%, back to where it was at prior market peaks in January 2018 and May 2007. Not coincidentally, both of those times were just prior to significant stock market declines. The Investors Intelligence survey showed the bull camp at 63.6%, while the bear share dropped to 16.7%. Almost four bulls for every bear! Meanwhile the bull/bear spread, at 46.9 percentage points, was beyond extreme levels. The retail investor American Association of Individual Investors (AAII) poll moved to 52.7%, well over double the 23.4% share in the bearish camp. Those are only the sentiment indicators which measure what investors think about the outlook. In terms of how investors are positioned in the market, the reading are even more extreme. The household sector financial mix was over 70% in equities, as individual investors refused to rebalance and take profits this cycle. This took out the bubble peaks in both 2000 and 2007. The sell-off did take some of those extreme sentiment readings lower, but we also will be curious to see if the sharp bounce back will also re-embolden those bullish views. Moreover, the decline was so brief that there was probably not much time for investors to do a major asset reallocation , suggesting that investors are still fully invested on the stock side. While many were pushing ‘panic buttons’ during the sell-off suggesting the Fed may actually have to move on interest rates prior to the September meeting, we see little chance of that but do note that short-term interest rates are more than 200 basis points above a neutral level, so there is certainly lots of room for a 50 basis point move in September as the Fed would ‘front load’ the easing cycle a bit. Upcoming readouts on the U.S. labour market, including the monthly payrolls report, will give Federal Reserve policymakers insight into the need for further interest-rate reductions after an all-but-certain cut in a little more than two weeks. A cut of only twenty-five basis points might disappoint stock investors though, especially since valuations (as seen below) have climbed right back up towards the highs of late 2021, which were eclipsed only by the massively excessive technology-lead valuations of the late 1990s.

North of the border here, Canada’s economy grew faster than expected in the second quarter. But the most recent report also pointed to economic weakness over the summer, keeping further interest rate cuts by the Bank of Canada clearly in view. Despite the elevated pace of growth in Q2, the third quarter is likely to drop off and fall well below the Bank of Canada’s 2.8% forecast. Industrial growth showed a flat June monthly reading, with resources declining. Add in the short but impactful rail stoppage in August and third quarter growth will probably only be about 0.25%. The central bank is unlikely to opt for outsized cuts, though, as it lowers borrowing costs, according to a new Bloomberg survey. In fact, none of the 18 analysts who responded to the poll believe the bank will reduce the policy rate by 50 basis points or more at any meeting. Rather, the majority see five cuts of 25 basis points at the next five meetings, until the benchmark overnight rate is at 3.25%. Governor Tiff Macklem has already cut twice to lower the policy rate from its 5% peak. The survey suggests forecasters are optimistic about a gradual normalization of monetary policy, consistent with a soft landing for Canada’s economy.

We have not made any adjustments to our economic outlook. We had been expecting weakness for more than a year, but this had been delayed due to huge pandemic savings and a very favourable fiscal spending backdrop, particularly in the U.S. Those tailwinds have faded recently though, and we see the U.S. catching up on the downside to the rest of the global economy. Higher interest rates are finally having their ‘long and variable lagged’ impacts on consumer spending since firms and households locked in low interest rates during the Covid pandemic and had thus far only seen the positive impact of higher interest rates on savings as opposed to the negative results when loans and mortgages have to be rolled over at much higher interest rates. In fact, about 95% of current 30-year mortgages are locked in at an average interest rate of 3.9%, while the current 30-year rate is over 6.5%. Investment-grade companies also locked in lower rates on their debt. Consequently, rate hikes didn’t have the textbook negative impact on the economy. Another big factor supporting this economic resilience is due to ‘wealth effect’ from the gains in both the stock market as well as housing. With the stock market valued at a record 160% of gross domestic product in the U.S. the ongoing gains have emboldened consumers who now feel wealthier to continue spending, even if those are only ‘paper (unrealized) gains. The worry here is that this has become a ‘self-fulfilling prophecy’ and therefore presents a higher risk to economic growth if stocks pull back.

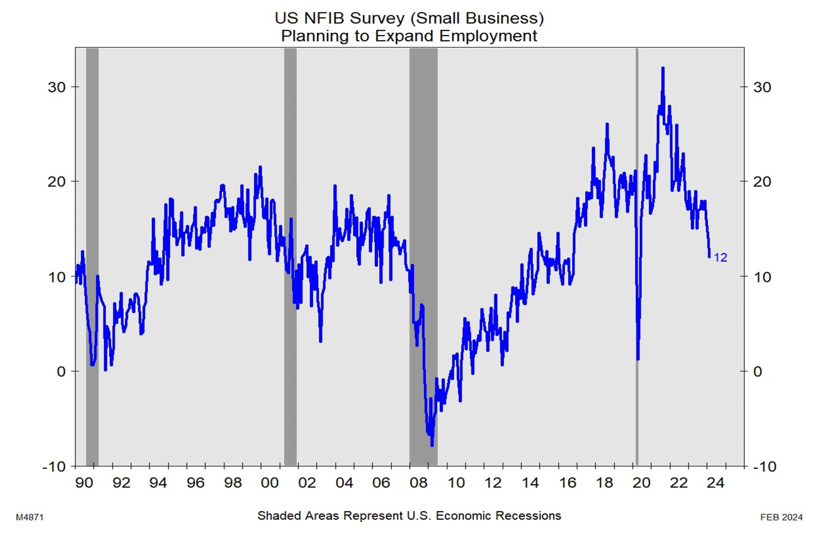

Meanwhile, consumer spending outlays have outstripped disposable income for most of this year, even as consumer savings have dwindled. In July, real personal disposable income rose 0.1% for the second consecutive month, the BEA reported. The U.S. personal saving rate ticked down to 2.9% on a year-to-year basis from 3.4% in June, representing a two-year low and less than half of the 7% rate it was early in the pandemic. As a result, many economists now expect consumer spending to slow, particularly if employment conditions weaken, as expected. We are seeing clear signs of this financial stress at the low-end of the income scale. Dollar General is the latest to report slowing sales and cutting their guidance — and it’s a discount store no less (the stock price collapsed a record -29% following that report and comment). The CEO cited “financial constraints” among their core customers and, of course, called for more promotional activity. “Our core customers are often among the first to be affected by negative or uncertain economic conditions and among the last to feel the effects of improving economic conditions.” The majority of these “core” customers, who constitute the lower end of the income scale, “state that they feel worse off financially than they were six months ago as higher prices, softer employment levels, and increased borrowing costs have negatively impacted low-income consumer incentive.” Employment has been a big driver of strong consumer spending as jobs had been plentiful. That has clearly begun to change as employment growth decelerates and we must look no further than the small business hiring plans chart to see how this downturn has evolved and the fact that each prior time we saw such a slowdown, the economy ended up in recession (grey area on chart).

In Canada the big story in August was the reporting of third quarter earnings by the major chartered banks. Investors had been ready for poor results and year-over-year declines in net income since most banks were expected in to increase loan loss provisions. But the results came in surprisingly strong in almost all cases with some increases in loan loss provisions being offset by higher capital markets returns as banks continue to benefit from strong stock markets, trading activity, corporate finance and wealth management. Only the Bank of Montreal came in well below expectations (for the third consecutive quarter) and significantly increased their provisions for bad loans. Whether they are just being more conservative (and honest) in their assessment of risks than the rest of the banks or are really experiencing a much worse result in lending may not be known for a few more quarters, but the lender stood out by having an unexpectedly high level of loan-loss provisions and an explanation for them that left investors dissatisfied. BMO said it made bad-loan provisions of $906 million, up from $492 million a year earlier. While five of Canada’s six big banks provisioned more in 2024′s third quarter than the year before, BMO’s increase of 72% was easily the largest. This might be tied to the massive purchase last year of Bank of the West in the U.S. and higher provisions to appease U.S. regulators and avoid problems similar to what we saw when TD Bank was targeted by regulators for AML (anti money laundering) shortfalls and subsequently denied completing their $20 billion announced purchase of First Horizon Bank in Tennessee. By contrast, Royal Bank of Canada and Canadian Imperial Bank of Commerce (CIBC) impressed Bay Street analysts and investors by highlighting the credit quality of their loan books, and how relatively little they had to set aside for future problems. National Bank also beat expectations on strong capital markets activities.

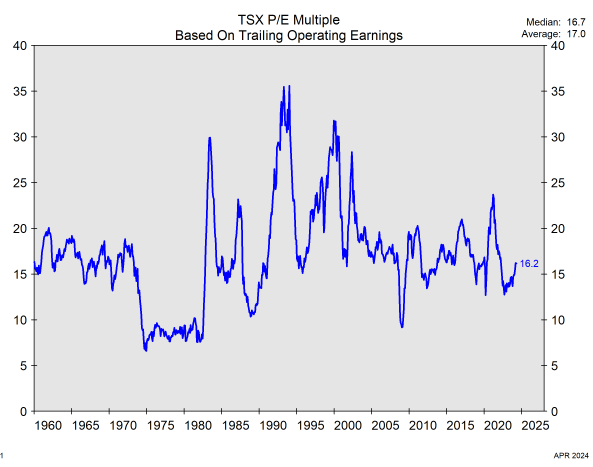

Bottom line for the Canadian banks was that the results were good in an increasingly tough economic environment. Given that the performance of the bank stocks so far in 2024 has lagged the non-bank financials (i.e. the insurance companies) as well as comparable U.S. banks, there might be a bit of a ‘catch up’ trade ahead for the Canadian banks to narrow that gap. At the very least, they should hold up relatively well in case of any stock market weakness since the valuations are low and they all have strong support from dividend yields. Since the banks are such a large part of the overall Canadian market, they have kept the valuation of the entire market closer to the mid-point of the long-term average (see chart below) as opposed to the U.S. market, which is still trading near record valuations, buoyed by the excess valuations of the large technology stocks.

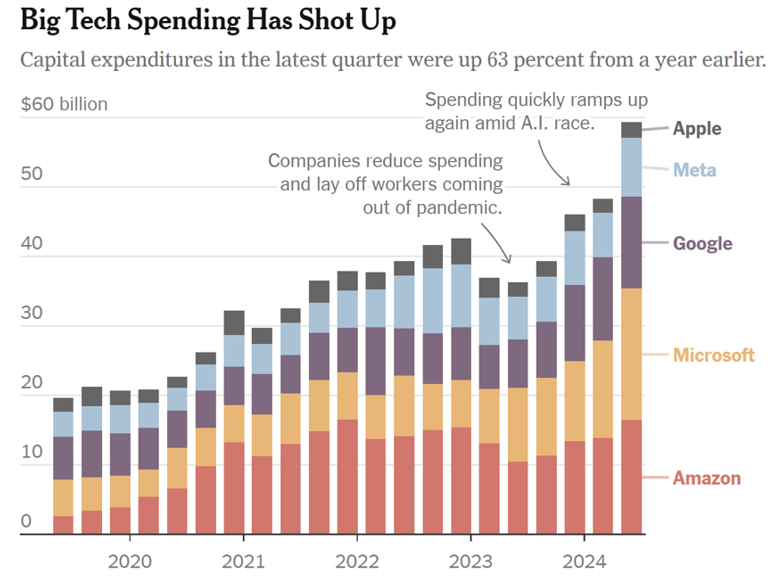

Meanwhile in tech world, we are in the midst of the greatest Capex super cycle in recent memory. Demand for semiconductors, specifically Nvidia’s GPUs, is far outstripping supply as an immense amount of compute capability is required to power this new technology. Hyperscaler spending is still on track with $50+ billion annualized quarterly spending just reported and NVDA still getting over 80% of that business. Artificial intelligence (AI), like the internet in the early 2000s, presents new sales and profit opportunities for both Big Tech and the smaller players. Tech’s heavy weighting in the S&P500’s market value pulled the benchmark index up 52% since its October 2022 low. But the differences between now and then are significant. The largest AI gainers, such as Nvidia, Microsoft, Meta Platforms and Alphabet, are some of the most profitable companies on the planet; the internet companies were losing money. Also, today’s innovators have clear competitive moats around their businesses. In their own recent earnings reports, Microsoft, Amazon, Meta Platforms and Google’s parent, Alphabet reported combined capital spending of $58.5 billion just for the June quarter—up 64% year over year. All four projected that spending would stay elevated this year and into next, and all pointed to “AI infrastructure” as the main driver. That has been great news for Nvidia, which commands the lion’s share of the AI chip market. But the durability of that spending is still a question—especially if actual demand for generative AI services doesn’t materialize at the pace that tech optimists currently envision.

Nvidia was the big story in technology in August as it was the last of these major tech companies to report earnings. The shares fell on about 6% after their earnings release last week, as the company’s fiscal second-quarter gross margin dipped slightly, and its revenue beat was eclipsed by a backdrop of increasingly lofty expectations despite being up 122% year on year. It was the fourth straight quarter of triple-digit revenue growth. Large technology companies have been ramping up investment and buying Nvidia’s graphics processing units to train large AI models. But as Nvidia continues its rapid expansion, the annual comparisons are getting tougher even as they issued market-beating revenue guidance for its fiscal third quarter of $32.5 billion, implying an 80% year-on-year increase, but a slowdown from the July quarter. Meanwhile, the company said that gross margins would be in the “mid-70% range” for the full year. Analysts had been expecting a full-year margin of 76.4%. The new products that Nvidia is building to stay well ahead of the competition are rising significantly in complexity—weighing a bit on the company’s gross margin line. Nvidia’s gross margin of 75.1% for the most recent quarter was down 3 points from three months earlier, but well above the 65% the company has averaged over the past four years. And even at 75%, Nvidia is commanding a higher gross margin than all but one of the other companies on the PHLX Semiconductor Index. But given the exceptionally high market cap to revenue ratio (over 30 times) the stock is trading at, high margins have clearly been the biggest factor supporting high earnings growth. If more competition and some slowing of capex by its customers is leading to more price pressures, then the stock could be even more volatile and have downside risk. But, for now, the next few quarters at least look like strong growth with continue.

So how does all this impact our investment strategy for the balance of 2024? While we entered August with stock weights near the bottom end of our typical range, we did add back on the early month sell-off, particularly in the tech and financial sectors. Bonds no longer look particularly attractive to us. While we have not reduced the allocation to fixed income, we have substantially reduced the terms of our bond holdings, selling mid- and long-term bonds and replacing them with shorter term bonds in the 2-3 year maturity range. We expect the yield curve to ‘normalize’ over the next year, meaning that short-term interest rates should drop (probably 150-200 basis points) but we see very little room for further declines in longer-term interest rates unless the economy deteriorates much more than is current expected. Cash is still providing a strong yield but that will diminish as short-term interest rates fall. So, by default, stocks still look like a preferred alternative to cash, longer-term bonds or preferred shares (where we have some concerns about deteriorating credit conditions). However, we still have serious concerns about slowing economic growth and overly optimistic earnings projections so continue to see sector and stock selection, rather than broad market exposure, as the key to generate superior returns. Our sector overweight positions are in the groups which have low economic sensitivity, some leverage to falling short-term interest rates, low valuations and dividend yield support. This argues for continuing to hold stocks in the telecom, utilities, pipeline, health care and financial sectors. We also continue to hold a significant, though underweight, position in technology stocks with a focus on the larger names including Meta, Alphabet, Amazon, Nvidia and Micron Technology (recently added on the early August weakness). Also, with the substantial weakness we saw in the U.S. dollar last month, we continue to like the outlook for gold, particularly the mining stocks, which have continued to lag the gains in gold bullion.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.