Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

August 7, 2024

Bonds enjoyed good returns in July as investors became more confident that interest rates would move lower over the balance of this year and next. The expectations of lower interest rates caused bond yields to move sharply lower, particularly for shorter term issues. Better than expected inflation data combined with some weakening of labour markets led both the Bank of Canada and the U.S. Federal Reserve to sound dovish following their respective rate setting meetings in the month, which seemed to validate investors’ optimism regarding rates. Geopolitical uncertainty in the Middle East also contributed to the rally because it prompted a flight-to-safety bid for bonds. The Bloomberg Canada Aggregate and FTSE Canada Universe indices earned 2.23% and 2.37%, respectively, in the month. As a result, the year-to-date returns of both indices finally turned positive.

In Canada, the key piece of economic data was lower than expected CPI inflation. In July, we learned that prices unexpectedly declined 0.1% in June, and the annual rate decelerated to 2.7% from 2.9%. The unemployment rate rose to 6.4% from 6.2% despite a drop in the participation rate. Higher unemployment reflected ongoing population growth while job creation stalled. In addition, weaker than expected retail sales suggested consumers were struggling to manage higher interest rates and past inflationary pressures. On a slightly more positive note, the Canadian economy continued to grow at a pace slightly above 1.0% per annum. Hardly a robust pace, but not a recession either. The Bank of Canada followed up its June 5th interest rate reduction with a second 25 basis point cut on July 25th. The Bank’s next rate setting meeting will be September 4th.

Economic news in the United States was mixed. Growth in the second quarter was estimated at an annual rate of 2.8%, well above both the 2.0% forecast rate and the 1.4% pace of the first quarter. Industrial production was stronger than expected due to a manufacturing rebound and retail sales beat forecasts. However, the unemployment rate rose to 4.1% from 4.0%, and surveys of manufacturing and service industries suggested activity was slowing. Importantly, U.S. inflation slowed more than expected, to 3.0% from 3.3% a month earlier. The Fed left its interest rates unchanged at its July 31st meeting, but noted it was monitoring both its employment and inflation mandates, which many observers believed was a hint that there would be a possible rate cut at the Fed’s next announcement on September 18th.

Internationally, most central banks were leaning toward reducing interest rates, but did not act in July. As this is being written, however, the Bank of England has narrowly voted (5-4) to lower its rates by 25 basis points, its first reduction this cycle. The Bank of Japan remained an outlier, as it raised its interest rates by 20 basis points in late July and indicated that it would gradually reduce its bond purchases (also known as quantitative easing) over the next two years. The Bank of Japan also intervened in the foreign exchange market to bolster the Yen, which had declined sharply to its lowest level in 38 years. As a result of the intervention and the interest rate increase, the Yen rallied finishing the month with a 7.1% gain.

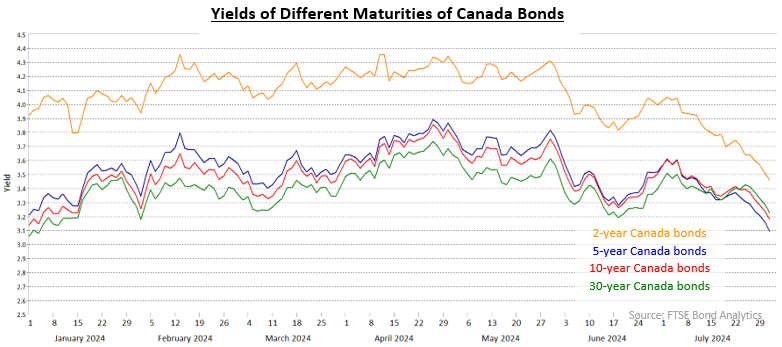

Yields of shorter term bonds fell significantly more than those of longer maturities in July. The yield of 2-year Canada bonds dropped 54 basis points in the month, while 30-year yields fell 17 basis points. Yields of 5-year and 10-year Canada bonds declined 42 and 32 basis points, respectively. As a result, the Canadian yield curve inversion began disappearing, with 10-year Canada bond yields finishing above 5-year yields, and 30-year yields closing above 10-year ones. The yields of 2-year Canada bonds, though, remained higher than those of longer maturities reflecting the Bank of Canada’s relatively high overnight target rate. The decline in mid and long term yields brought them back down close to where they began the year. Only 2-year yields have seen much change from the start of the year, reflecting the Bank of Canada’s two rate cuts.

Although the Fed had yet to begin lowering interest rates in the United States, the changes in U.S. Treasury yields during July were remarkably similar to the changes in Canadian bond yields. The yields of 2-year and 30-year Treasuries dropped 52 and 14 basis points, respectively. By month end, the U.S. yield curve from 2 years to 30 years was positively sloped.

The federal bond sector gained 2.25% in the month as the sharp drop in yields resulted in higher bond prices. The provincial sector returned 2.62%, benefitting from the longer average duration of those bonds. Provincial yield spreads were little changed due to significant new issue supply. Investment grade corporate bonds earned 2.23% as good investor demand caused their yield spreads versus benchmark Canada bonds to narrow 4 basis points. Non-investment grade corporate bonds earned 1.34% in July as their shorter average durations and weakness in Corus Entertainment bonds reduced overall returns. Real Return Bonds gained 3.48% with investors apparently shrugging off the better than expected inflation news. Preferred shares enjoyed another strong month, earning 2.25% thereby keeping pace with bonds in July.

We believe both the Bank of Canada and the Fed will lower their respective interest rates at their next meetings in September, barring an unexpected rebound in inflation. Canadian growth has been struggling for close to a year and, as a result, the economy is no longer operating at full capacity. In the United States, the economy has been stronger, but the pace of growth has slowed somewhat. In addition, as this is being written, the U.S. unemployment rate has jumped to 4.3% from 4.1% due to job creation slowing while more people entered the labour force (the participation rate moved higher). The market had been already anticipating a September rate cut by the Fed and this news all but guarantees that will happen.

The interest rate reductions to date by the Bank of Canada and the future ones expected of both the Bank and the Fed mean the yield curves in both countries will normalise with shorter term yields moving lower than longer term yields. We have structured the portfolios to benefit from this change in the yield curve by increasing the mid term exposure and reducing the holdings of very short and very long term securities.

We are less certain about the level of overall yields, however. In past market cycles, mid and long term bond yields have fallen as the Bank of Canada has lowered interest rates, but in this cycle those yields are already much lower than the Bank’s overnight target rate. We believe the market may be anticipating more rate cuts than will occur, which means mid and long term bonds may not rally much from current levels. Accordingly, we are keeping portfolio durations close to neutral, rather than extending them.

Corporate credit yield spreads are relatively tight despite economic slowing that is causing central banks to ease monetary policy by lowering interest rates. We also observe that equity markets, particularly in the U.S., have rallied on the performance of relatively few large cap stocks. In the event of an equity pullback, we would expect corporate bonds to weaken versus government issues. We are, therefore, maintaining the allocation to the corporate sector at close to the benchmark level, awaiting better opportunities to increase the corporate holdings.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.