Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 2, 2024

As fully expected, the U.S. Federal Reserve left interest rates unchanged at the meeting that ended today but left the door wide open for cuts to begin. Exactly a year after its last rate hike, a good run of economic data has the Federal Reserve closing in on its first cut since March 2020, but it’s still not clear when it will happen. Markets are more than 100% certain of a quarter-basis-point cut in September. Stocks rallied again in July but the biggest difference from the other rallies so far this year is that the gains were far more widespread, with small cap and ‘value’ stocks leading the charge while we saw some weakness in big cap tech, despite relatively good earnings reports from those prior leaders. Amazon, Meta, Microsoft, Alphabet, Apple and Tesla were all down 10-15% from peaks earlier in the month while the ‘top dog’ Nvidia dropped over 20% from its early July high, shaving off an astounding $1 trillion in its market cap, almost double its entire market capitalization at the beginning of 2023! Meanwhile, the small cap Russell2000 Index was up over 12% on the month, driven in large part by prior laggards such as financials and energy. Canadian stocks also did better for a change, rising over 4% for their best month since the fall of 2022 and contrasting nicely with the flat monthly results for the S&P500. The catalyst for the most recent rally appeared to be the consensus view that the U.S. Federal Reserve is finally ready to start taking interest rates lower, prompted both by continued good news on reducing inflation as well as much softer economic data. Since the small cap stocks in the Russell2000 have a much higher overall debt level and more domestic market exposure than the bigger international companies, they stand to benefit more from the cut in interest rates. Valuation in those sectors is also significantly more depressed than the large growth stocks and their overall weight in retail portfolios and most index funds is also far less so the shift of even a small percentage of money from the big index growth stocks to the small cap sector tends to result in more pronounced price moves. The same thing happened in the ‘everything rally’ during the 4th quarter of 2023. However, in that case, the momentum faded, and the big growth/tech stocks took the lead again this year, mostly because the earnings results from those smaller sectors did not support the stock gains but big tech continued to deliver strong earnings growth from the ongoing AI infrastructure buildout. The ‘jury is still out’ on whether that will occur again following the July gains. The third quarter earnings reports that we see over the next few weeks from the regional banks, retailers and manufacturing companies will help to define that next move but, with the overall macro-economic data still in decline, we are sceptical that these recent gains can hold. The bottom line for our investment strategy is that we are sticking with our neutral weight on stocks in client portfolios but have shifted the mix of the stock sectors to favour those that have higher dividend yields (to benefit from falling short term interest rates), moderate valuations (due to downside valuation risks) and earnings with less economic sensitivity (due to slowing growth). Utilities, pipelines, telecom and some parts of technology all fit this profile.

What keeps us up at night? The biggest and hardest lesson learned after over forty years of money management is that the best long-term strategy is to stay invested, stick with quality growth stocks and not trade too actively. I recall doing one of my first group speaking engagements at an investor conference back in 1985. I wanted to project a very positive, bullish image, so I opened by pointing out the exciting news that the Dow Jones average had just hit a record high of 1500. Today it is above 40,000, which measures as an average annual return of 9% over that entire period. Clearly just staying invested throughout all the good and bad times generated strong results without trying to guess when it was a better time to be in or out of stocks. Moreover, those results are for the Dow Jones Industrials Index, and we know that other indices such as the Nasdaq100 or the S&P500 have done even better over that same time frame. But we have also seen six significant downturns over that period with drops of anywhere from 20-50% and know how devastating those declines can be and how they can impact retirement decisions and other important spending considerations for investors. We therefore like to be aware of signs that shorter-term risks have increased, and we might want to get more ‘defensive’ in our portfolios positioning, without necessarily getting out of stocks altogether. We are seeing many of those signs today. The ‘lack of breadth’ in the market gains over the past two years is well documented and certainly seems to be a primary risk and continues to be a concern for us. We have just 25% of individual stocks beating the index year-to-date, which also is an unprecedented degree of underperformance dating back to 1974. In fact, five stocks alone accounted for over 35% of the overall gains in the S&P500 in the first half of 2024. Increasing breadth is the hallmark of any sustainable bull market, so the narrowness here does not bode well for the overall outlook.

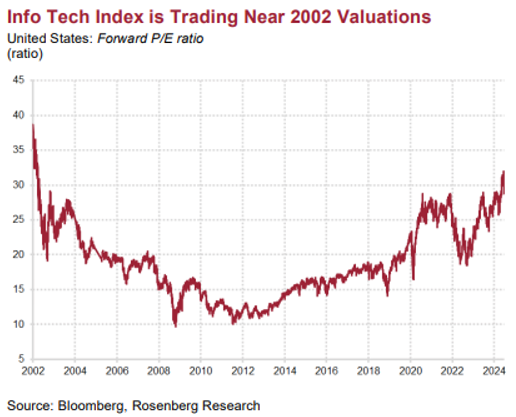

Valuations are also a concern. While many pundits will point out that these valuations are still below the excess levels since at the peak of the ‘tech bubble’ in 2000, we are certainly closing in on those levels again. Also, at that time, many strategists said that we would not be likely to see such on overvalued market again in our investing lifetimes or, as it turns out, almost 25 years later! On top of that, the gains in the market have been driven almost solely by higher levels of valuations, as opposed to real earnings growth. Since the beginning of the year, the consensus forecast on 2024 S&P500 composite earnings has risen from $243 to the current level of about $245, an unimpressive gain of under 1%. For 2025, earnings projections have risen less than 2.0%. Meanwhile, the stock market is up +17%, meaning that only 15% of the gain in the price has come from any improvement in the earnings outlook. Clearly, stocks are reflecting a lot of optimism that the Federal Reserve will move quickly to reduce interest rates back to a neutral level and that these moves will give an economic lift to the interest sensitive sectors of the economy, particularly housing.

While valuations alone are not a reason to expect a pullback in stocks, there are also other speculative activities going on that are reminiscent of prior peaks. The return of ‘meme stocks’ is one such indicator of excessive risk taking. But we are also reminded of the catalyst for the eventual collapse of the technology bubble in 2000, which was the excessive valuations of companies that were investing in internet infrastructure (called PPE or Property, Plant and Equipment) at that time. Companies were getting valued in the stock market at ‘multiples of PPE’ which just encouraged them to continue to raise capital at those excessive valuations and put the money into more PPE. The sellers of PPE (i.e. the datacom equipment companies such as Nortel, Lucent, Cisco and JDS Uniphase) were the big winners in that scenario, not unlike the way the providers of AI infrastructure (the semiconductor companies…..mostly Nvidia) have been the big winners in the past two years. Once the spending started to slow down, investors found that the valuations had no support, and it became an investors ‘game of musical chairs’ as to which stocks would survive. While we may not be at that stage yet in the AI rollout, the warning signs continue to increase.

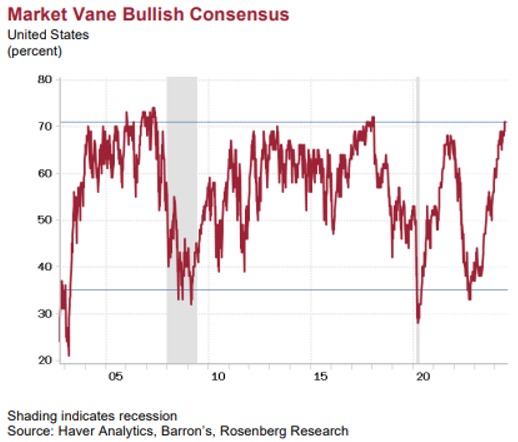

Another worry it that investor sentiment is very extended, and investors are ‘all in’. Key market sentiment measures are ‘off the charts’ exuberant. The Market Vane weekly Bullish consensus is now at 72% — back to where it was in January 2018 and before that in May 2007. Not coincidentally, both of those times were just prior to significant stock market declines. The Investors Intelligence survey shows the bull camp at 63.6%, while the bear share dropped to 16.7%. Almost four bulls for every bear — the bull/bear spread, at 46.9 percentage points, is now beyond extreme levels. This ‘herd mentality’ seems now to be viewed as a reason to pile in as opposed to how this metric was viewed in prior cycles — a sign that all the good news is already priced in and there is nowhere to go but down. The retail investor AAII poll just moved above 50%, to 52.7%, in the latest week (from 44.4% a month ago), which is well over double the 23.4% share in the bearish camp. Those are only the sentiment indicators which measure what investors think about the outlook. In terms of how investors are actually positioned in the market is even more extreme. The household sector financial mix is now over 70% in equities, as individual investors refused to rebalance and take profits this cycle. This takes out the bubble peaks in both 2000 and 2007. It is also somewhat an unheralded risk for the retiring baby boomer community, with over 60% of their asset mix is in equities, are double where they should be at this stage of their life. Coupled with that is the fact that over half the stock market today is in passive indexed funds, so we have double concentration on our hands — extreme concentration of equities on individual balance sheets, and within that equity tranche, the most concentration in a handful of stocks that we last saw during the last Tech mania in the late 1990s, and we know how that turned out. One final interesting but completely non-statistical piece of information was the recent announcement that JPMorgan’s bearish chief global strategist Marko Kolanovic will “leave his role” where he was employed for 19 years. Was this the price to be paid for calling for a -25% decline in the S&P500 this year? Just as you always look for the biggest bulls to be retired in a bear market as a sign that the worst is over, this seems to be a tell-tale sign that there is no room for contrarian views on Wall Street today.

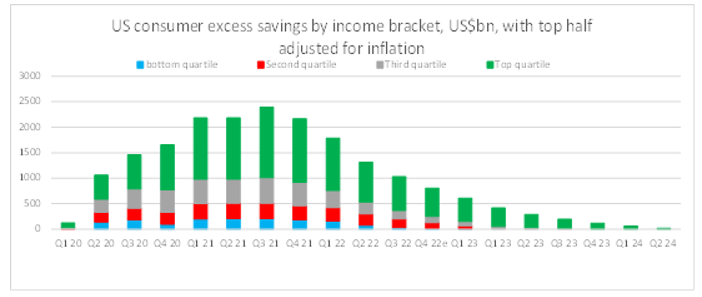

A final concern is that the economic data has clearly rolled over, and this presents a problem both for employment levels as well as corporate profits. On the macroeconomic front, ISM manufacturing and services are now both below 50, the demarcation line between expansion and contraction, with manufacturing at a 4-month low, and services at a 4-year low. More fuel for the slowdown thesis from weekly employment claims, which are a better leading indicator than payrolls and dismal readings from U of Michigan Consumer Sentiment Surveys, which were well below expectations and back down to 2-year lows. We have also seen a major spike in bankruptcies (up 100% year-over-year in Canada) and ongoing increases in credit delinquencies on both side of the border. Higher interest rates are finally having their ‘long and variable lagged’ impacts on consumer spending. The costs to borrow for a home, a car or on a credit card are at the highest levels in decades and the total amount of interest consumers paid on mortgages in 2023 rose 14% from a year earlier, according to Bureau of Economic Analysis data. It jumped 50% for other types of consumer debt, such as credit cards and auto loans. Households have relied more on credit cards, and more have carried balances month to month. Balances rose to more than $1.1 trillion in the first quarter, New York Fed data show. That number was the second-highest balance on record, after the fourth quarter of last year, and an increase of around a third compared with 2022. The chart below shows how consumers have used up the excess savings accumulated during the pandemic, with almost no savings accumulated now in all but the highest income brackets. No wonder then that we have seen such a pullback in consumer spending this year and such sober outlooks from many of the consumer products companies in their earnings calls.

The U.S. consumer has really been the ‘last man standing’ in terms of the retreats in the global economic data since the rate increase cycle began in 2022. If it wasn’t for the enhanced AI excitement and the late cycle fiscal spending and monetary stimulus in the U.S., we believe the world would already be in recession and we’d probably be in a global bear market in stocks. The U.S. labour markets are no longer travelling from ‘too tight’ to ‘just right’, with the accompanying market supportive expectations of Fed cuts and a soft landing. They are now heading from ‘just right’ to something worse as downside economic momentum takes firmer hold. The danger here is that the U.S. overshoots the inflation target on the downside and tips into deflation. At that point we will find out that bad news on the U.S. economy becomes bad news for U.S. stock markets. Second quarter earnings reports are now bearing out the slowdown story we have been seeing in the macro data and ‘Economic Surprises Index.’ From Visa to Pepsi to Nestle to Gucci to Ford to Starbucks to Nike and to LVMH the story seems to be the same; the consumer is tapped out and pulling back on spending. Even McDonalds missed estimates and guided down, further demonstrating that growing weakness is spreading to even the ‘value conscious’ segments of the market. Other negative outlooks in leading sectors include Tesla, Ford, Stellantis and General Motors all seeing EV demand dry up and inventories soar. Also, what is more economic-sensitive than UPS and look what happened in its just-completed quarter, with average revenue per domestic package deflating -2.6% on a year-over-year basis for the second straight contraction. This is all emblematic of a problem, and it is not with inflation, which is the ‘rate of change’ in prices. That has clearly come down. The problem is the elevated level of consumer prices in general. Consumer prices have shot up +22% in the past four years which has not happened in four decades. At the same time, wages have only risen +18%, leaving the “average” household moderately in the hole in real purchasing power terms

Sticking with technology for now but at a lesser weight as we are concerned about some issues ‘bubbling’ up. We had taken some profits in some of the high profile names in the technology sector, including chip stocks AMD and Nvidia as well as hyper-scaler Meta since we believed that it would be very difficult for those companies to meet elevated expectations for earnings in the upcoming reporting period and, even if they did hit those numbers, we had seen stocks sell off on those results regardless. Alphabet last week was a classic example of this as investors focused more on their continued elevated spending on AI infrastructure and their ability to monetize that spending as opposed to the actual results, which beat expectations on almost all metrics and showed continued growth. Investors have moved from the excitement over the growth in spending on AI to the question of when this massive spending for AI infrastructure will yield profitable returns to justify continued spending. Microsoft said it would spend more money this fiscal year to build out AI infrastructure even as growth slowed in its cloud business. Microsoft said its capital spending rose 77.6% to $19 billion in its fiscal fourth quarter that ends June 30, with cloud and AI-related spending accounting for nearly all the expenditures. Google warned last week that its capital spending would stay elevated for the rest of the year. While this is all very good news for the providers of this infrastructure (primarily Nvidia), when these initial massive spends slowdown will it be like the gap in the tech sector we saw in 2000 once the initial buildout of the internet had taken place and the applications were now needed to profitably grow and fill that gap. On that count we have seen mixed data. The proportion of global companies planning to increase spending on AI over the next 12 months has slipped to 63% from 93% a year earlier. Potentially quantifying the AI bubble is a calculation by Silicon Valley venture-capital firm Sequoia that the industry spent $50 billion on chips from Nvidia to train AI in 2023 but brought in only $3 billion in revenue. Artificial intelligence has not significantly impacted firm productivity yet and will continue to have a minuscule effect for a long while. According to a recent NBER paper, the developments from artificial intelligence will only increase measured total factor productivity by a mere 0.66% in the next 10 years. The latest Business Trends and Outlook Survey from the Census Bureau shows that only 5% of companies in the U.S. are using AI — an extremely low number given the hype around the technology. Regarding AI applications, the most used are in marketing automation (2.5% of U.S. companies) and virtual agents (1.9%). Other applications of AI are not working their way into business processes yet, with only 1% of firms using large language models. On top of the industry growth risks we have also seen increased selling of these large growth stocks from insiders as well as hedge funds

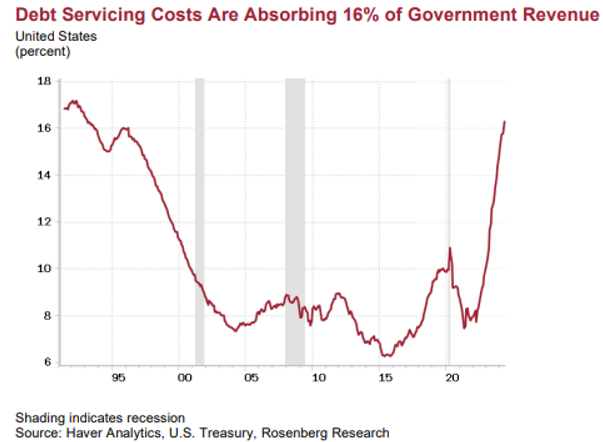

Why aren’t we more bullish on bonds? With our admitted weak economic outlook and belief that the path of interest rates over at least the next two years will be downward, we are not particularly positive on mid and long-term government bonds nor the corporate bond sector. While we do expect central banks across the globe, but particularly in North America, to be cutting short-term interest rates aggressively, we don’t believe that same reduction will take place in the longer end of the yield curve. In fact, we expect that long-term rates will only drop marginally or might even stay at current levels while short-term interest rates fall as much as 200 basis points. This will tend to ‘normalize’ the yield curve, meaning that short term rates will be the lowest and that rates at longer maturities will be higher, the opposite of what exists today which is a highly ‘inverted yield curve.’ The primary reason for this is due to the massive government borrowing required, particularly in the U.S. to fund the ongoing record levels of government debt. Investors will require higher ‘term premiums’ (i.e. the amount that long term yields exceed the inflation rate) to entice them to buy the massive amounts of debt that need to be funded in the public market. This also comes at a time when the two largest holders of U.S. debt (Bank of Japan and the Bank of China) have stopped buying. Moreover, chartered banks in the U.S. have been huge buyers of U.S. debt over the past few years and they have little room to add to those positions. In fact, the unrealized losses on holdings of government securities in U.S. banks is more than US$500 billion. The chart below shows how the debt surge in the past four years, along with the central bank’s tightening cycle, has sent interest costs up in the past year to $836 billion (about as much as the entire Pentagon budget) from $588 billion a year ago and about double the $423 billion interest expense two years ago. This will prove to be a serious constraint on both the economy and interest rates. In terms of the bond (or any other) market, a massive increase in supply combined with a decrease in demand is never a recipe for rising prices, even if short term interest rates are falling. Ergo, our less than bullish outlook on mid and long-term bonds and our preference for fixed income holdings with maturities in the 2-to-3-year range, which we view as the ‘sweet spot’ on the yield curve!

Investors missing a very important development when talking about ‘meme stocks.’ The chatter and the focus always centers around how high names like Gamestop and AMC can rise and is there value in those stocks? The answer to that question is easy. There is no value in those stocks at those inflated levels and you don’t have to go any further than asking the question, ‘have we ever seen private equity, probably the most astute and successful financial and operational buyers of assets, taking interests in these companies?’ The answer there is a ‘hard no!’ There is a more important development going on in our view and that it the ability of WallStreetBets and Reddit and other online platforms to consolidate a previously unconsolidated group of investors into a strong voting group. Whenever you can consolidate a diverse group, you can increase their power. This was seen in the early days of the union movement and its ultimate impact on wages and job security. So far, the ‘meme stock’ syndrome is all about who can make money on these stocks. The more important consequences of this consolidation of a diverse investment group may take a longer time to have a true market impact beyond these ‘headline grabbing’ short term moves.

In corporate news, the Canadian government approved Glencore PLC’s US$6.9-billion acquisition of the metallurgical coal business of Teck Resources, which they had been reviewing on both a net-benefit and national-security basis over the past eight months. There were some risks that the deal might not happen since Ottawa has stepped in to prevent deals involving the foreign acquisition of Canadian mining companies, most notable BHPs 2011 proposed buyout of Potash Corp on the grounds that it did not provide a ‘net benefit’ to the economy. With this deal now done, it effectively makes Teck a pure play on base metals, particularly copper with its massive Quebrada Blanca mine in Chile. This capital will allow it to expand further in base metals as well as supporting a substantial stock buyback. We expect Teck to begin to see a premium multiple as it joins the ranks of major global mining companies such as Freeport McMoran and we continue to hold it as a core resource position in client accounts.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.