Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

July 31, 2024

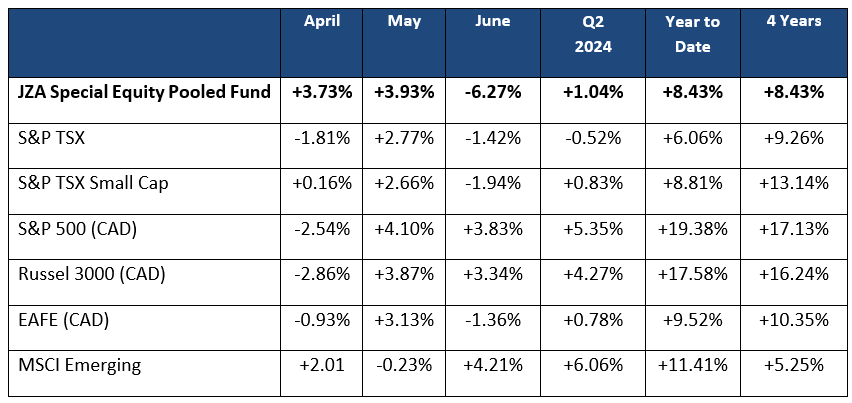

The second quarter of 2024 was a positive quarter as we moved forward with macro data showing inflation stabilizing somewhat. With this stabilization of inflation there is a continued expectation of a Fed rate cut in the back half on the year. On the back of this, we saw gold, copper and silver break out to new highs. With this backdrop, the portfolio was able to slightly outperform its benchmark in the second quarter of 2024. The portfolio return for the quarter was +1.0% versus the benchmark return of +0.8%. Below is a table with global returns both for the quarter, year to date and 4 years.

The best performing sectors in the portfolio last quarter were Financials +18.7%, Technology +9.9% and Materials +5.5%. The portfolio is significantly overweight both Materials and Information Technology which contributed to the portfolio’s outperformance. Both sectors were beneficiaries of rate cut expectations.

Energy -3.0% and Industrials -7.1% were the underperforming sectors this quarter. Energy’s pull back was partially related to OPEC providing a plan to bring on shut in production in the coming months/years, as well as muting the positive reaction in the first quarter from Canadian LNG coming on towards year end/ beginning of next year. As the summer approached it was quickly apparent that gas supply was far higher than what was needed, creating a downdraft in AECO pricing and pressuring gas weighted stocks.

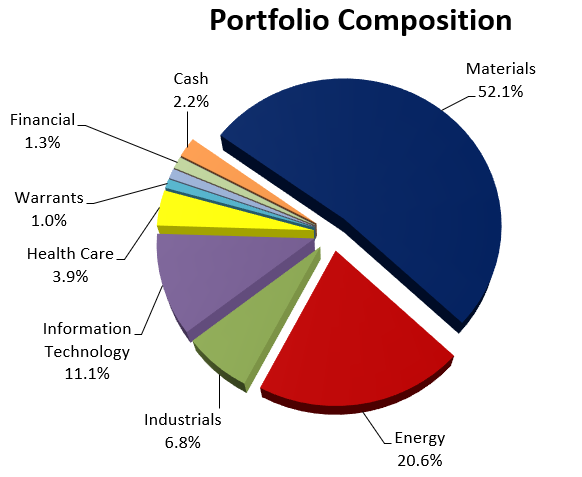

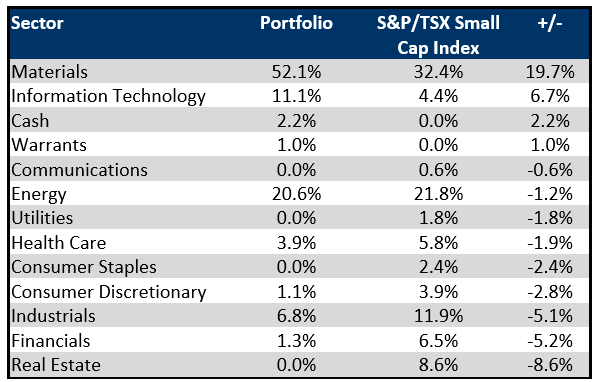

All in all, we were happy with performance in the second quarter. Below are two charts outlining the portfolios characteristics at the end of the second quarter in 2024.

In the second quarter the three stocks that detracted most from performance were Victoria Gold, Source Energy Services and Atex Resources Inc. Collectively these three positions cost the portfolio -1.5% in the quarter.

Victoria Gold was a position held in the portfolio with the expectation of improving their multiple as their cash flow improved after some operational issues last year. It is a single asset company and Victoria was the single largest private employer in the Yukon and represented 20% of provinces GDP. The Eagle Mine is an open pit heap leach operation located in the Yukon. On June 24, Victoria experienced a catastrophic failure of the leach pad causing it to shut down operations until a full investigation is conducted. At the completion of the investigation, unknown cost of remediation will be required as well as working with government agencies and first nation groups to hopefully resume operations. At the time the incident occurred, assessing the companies balance sheet we were concerned of the value that would remain for shareholders. We excited the position the day following the announcement. Unfortunately, this incident has impacted the value of Banyan Gold and Snowline Resources. We continue to hold these two positions as they are both exploration/development companies that are fully funded for their capital programs this year.

Source Energy Services produces high quality frac-sand from their Wisconsin and Alberta facilities to supply the Western Canadian Sedimentary Basin. Their long-life resource of sand is industry leading in terms of quality, reliability and reservoir conductivity. Further to their resource, the company has a well-connected network and state-of-the-art facilities to distribute to their clients. The main customer focus is Deep Basin, Montney and Duverney players. Historically the company has had higher leverage. Their current focus is profitability so it can deleverage and position itself for long-term sustainable growth. With the Energy sector weakness, Source Energy underperformed. We continue to hold this position and are looking for an opportunity to add to our holdings given our positive outlook for the company.

Atex Resources is a Chilean based copper/gold exploration company focused on their Valeriano project located in the Link Belt (region connecting the Maricunga gold porphyry belt to the El Indio high-sulphidation gold-epithermal belt which hosts significant copper-gold deposits) of north-central Chile. The company is focused on delineating and growing the copper-gold porphyry resource underlying a surface oxide gold deposit. The project is adjacent to El Encierro deposit, a joint venture between Antofagasta and Barrick Gold. As noted, we are very bullish on copper, and this represents part of the copper exposure in the portfolio. The company has strong supporters (Pierre Lassonde) and is well funded. Atex’s stock has been a strong performer year to date. The recent pull back follows the short squeeze on copper, and we believe is nothing more that a welcomed correction. We continue to hold the stock for what we believe will eventually be a sustained longer-term move in the copper price. There have been far too few copper discoveries to meet future demand and we continue to hold the Atex position.

The three positions in the portfolio which added most to performance included Reunion Gold, G2 Goldfields and Hudbay Minerals. Collectively the three positions added +2.0% to the portfolio. The portfolio continues to hold all three positions.

Reunion Gold has been one of our favourite gold explore company’s with their discovery and of the Oko West Gold Project in Guyana. Reunion has done a terrific job moving the company’s deposit forward and providing an updated Mineral Resource Estimate containing 5.9 million ounces of gold (indicated and inferred) at very good grades. We have felt for some time that this is one of the strongest return gold assets at the development stage in the world and this was recognized by G Mining when it made an offer to purchase Reunion on April 22, 2024 at a 30% premium. Given the quality of the asset and the chance of interlopers Reunion stock has done well in the second quarter. The gold price has also been strong, and the marketing of the merged company of G Mining and Reunion has brought many investors into both names. G Mining is a recognized builder of mines. The portfolio holds healthy positions in both stocks. Reunion will be spinning an explore co. out with the other land positions it holds, and the combined entity will most likely be added to the GDX in September.

G2 Goldfields follows along side the previous commentary. G2 Goldfields holds the property adjacent to Runion’s Oko West deposit. G2 refers to their deposit as Oka Main. The company is not as far along the delineation process as Reunion, but it is very evident that there is a significant deposit and will likely be developed with Reunion’s mine in some way shape or form. In January AngloGold Ashanti purchased an 11.7% stake in G2 Goldfields. For context Guyana was the world’s fastest-growing economy in 2022 (+62% GDP), is English-speaking with British rule of law, a parliamentary system and is considered mining-friendly with a straightforward path to permit. We continue to hold this position in the portfolio.

Hudbay Minerals Inc. is a proven builder/operator of long-life, low-cost assets in favourable jurisdictions with a bias towards copper production. The company is entering a period of significant production and EBITDA growth after completion of the Constancia expansion in Peru. The company retains a good growth pipeline for the future and has added to its production with the purchase of Copper Mountain in June 2023. Hudbay has had a tremendous move over the last year as it closes the valuation gap with its peers. Hudbay had lagged due to high capex and some operational issues. The gap has largely closed but with our positive outlook for copper, we continue to hold a position.

We feel like a broken record, but we continue to anticipate inflation to fall, which will allow the Fed to start reducing rates in the third quarter. Recent data has signalled unemployment is rising and CPI data falling. Our largest concern for the portfolio is for the Fed to lower interest rates too late causing the global economy to slide into a recession.

In a lowering rate environment, we continue to be bullish on gold and silver equities. As can been seen by the chart below, gold shares have only just broken out of a multi year base.

With the junior mining stocks (exploration and development) stocks just beginning to outperform their larger producing peers.

The portfolio continues to be overweighted the gold sector and exposed to great development projects that the larger producers will need to acquire to keep their pipelines robust. Our favorite holdings on the producing side are: G Mining, Alamos, Lundin Gold, Oceana and on the developing side: Snowline, Rupert, G2 Goldfields, Founders, Collective and Omai.

Although we have been wildly bullish on copper, we did not expect to see the short squeezes in April and May. Last quarter’s price action may be more financial manipulation than actual demand related but highlights the significant supply deficit and likely upward pressure on the price of copper once the global economy begins to recover. Although the graph below shows uninspiring Chinese demand for the red metal, when demand does pick up (which it will) the copper price is poised for significant upward momentum. Names of focus are Aldebaran Resources, Atex Resources, Hudbay Mining, Filo, NGex and Taseko.

Energy appears to be in a corrective phase but should outperform when interest rates fall. On sector weakness, we have been adding to the portfolio’s natural gas exposure (Kelt, Crew, Advantage and Spartan). Uranium stocks also continue to show strength. With the recent Kazatomprom news, the expectation for less uranium supply will lead to higher prices. We continue to hold Dennison, Nexgen Energy and enCore Energy.

In technology we continue to add names as some of our previous holdings have been taken out (Copperleaf and Nuvei). Two names we recently added is Real Matters and Sylogist. Real Matters in particular, should benefit from lower rates and an improvement in the housing market in the US. Another name that follows that theme is Adentra which wholesales hardwood lumber, plywood and related building products.

Finally, I was elected to the board of Wesdome Gold Mines Ltd, a Canadian gold producer listed on the TSX on June 18th, 2024. For context, I have found my work on the boards of PineCliff and Bonterra have given me unique insights into the operations of Canadian small cap energy companies, and it is my hope that by joining Wesdome, I will garner similar insight into Canadian gold stocks. The time commitment is minimal and will not interfere with my responsibilities and commitment to my portfolios and clients.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.