Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

July 7, 2023

The Canadian bond market struggled with higher yields and lower bond prices for much of June. In the end, though, a late rally in long term bonds offset declines in short and mid term issues and the broad market indices finished little changed in the month. The rise in bond yields came as the Bank of Canada resumed raising interest rates and the U.S. Federal Reserve paused but hinted at two future rate hikes. Inflation slowed but remained too high for the central banks to end their monetary tightening cycles. The Bloomberg Canada Aggregate index declined 0.03% in June, while the FTSE Canada Universe gained +0.04%.

Canadian economic data received in the month was somewhat mixed. GDP growth stalled in April, partly as a result of the federal employees’ strike, but StatsCan’s flash estimate for May indicated a rebound to 0.4% growth. The unemployment rate rose to 5.2% from 5.0% as 17,300 net jobs disappeared. The details of the labour market report were not as negative, however, as all the weakness was in the seasonally volatile youth segment (ages 15-24) which saw job losses of 77,000. In contrast, the prime segment (25-54) had robust job gains of 63,000 positions. As expected, the annual inflation rate dropped to 3.4% from 4.4% as the outsized increase in May 2022 was dropped from the calculation. Core measures of inflation did not improve as much and remained well above the 2% target.

The Bank of Canada resumed its monetary tightening on June 7th, raising its overnight rate by 25 basis points to 4.75%. It was the Bank’s first increase since January. The Bank cited concerns that inflation might get stuck materially higher than the 2% target as consumption and interest sensitive areas of the economy were stronger than expected and the labour market remained very tight. Bond yields, particularly for shorter terms, rose sharply following the Bank’s rate decision and investors began to consider the potential for additional tightening at the Bank’s upcoming meetings in July and September.

U.S. economic data released in June suggested that that economy was resilient despite substantial monetary tightening. The estimated pace of growth in GDP during the first quarter of the year was substantially improved from 1.3% to 2.0%, with consumption increasing more rapidly than previously thought. The unemployment rate rose to still very low 3.7% from 3.4%, despite surprisingly strong job creation. While pockets of weakness occurred in some business sectors, retail sales, housing starts, and construction spending were each stronger than expected. The annual inflation rate declined to 4.0% from 4.9%, but core inflation remained above 5.0%.

In June, the Fed paused its series of rate hikes, following 10 consecutive moves that increased interest rates by 5.00%. The U.S. central bank wanted to assess whether the lagged impact of the increases would be sufficient to slow the economy and bring inflation back to 2%. By the end of the month, though, strong economic data and sticky inflation pointed to further rate increases this year. Late in the month, Fed Chair Jerome Powell hinted that two more rate increases of 25 basis points were likely. The prospect of additional rate increases pushed bond yields sharply higher, particularly for shorter maturities. It also led to some weakness in the value of the U.S. dollar, but that may prove short-lived if the Fed resumes raising rates.

The Fed’s decision to pause raising interest rates was not contagious, as several central banks continued increasing their respective rates in efforts to dampen inflation. Notably, the Bank of England and Norway’s Norges Bank surprised observers when they both increased their respective rates by 50 basis points instead of the expected 25 basis point increment. The European Central Bank, the Swiss National Bank, the Reserve Bank of Australia, and Sweden’s Riksbank each raised rates by 25 basis points in June. Among major economies, only China lowered its interest rates in the month, as it tried to invigorate its economy following a disappointing rebound from its zero-Covid lockdowns. Weak Chinese economic data led to some commodity prices declining, which may be beneficial in reducing global inflationary pressures.

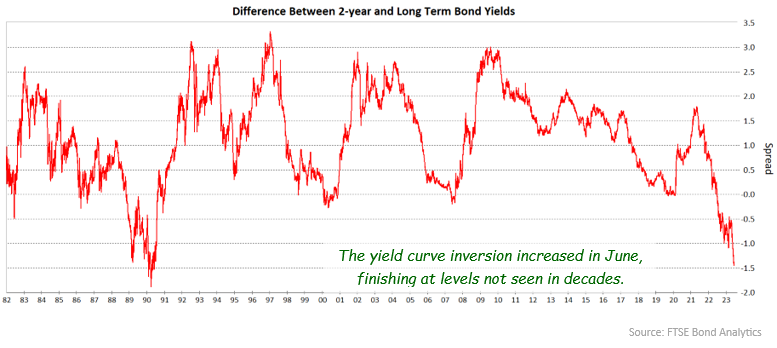

The Canadian yield curve inverted further as shorter term bond yields rose sharply in response to the Bank of Canada’s rate increase. That increase dashed hopes for rate reductions later this year and investors adjusted their expectations for yields staying higher for an extended period. Yields of 2-year and 5-year Canada bonds rose 36 and 24 basis points, respectively. Long term bonds experienced higher yields for most of June, but a late rally left 30-year yields 6 basis points lower on the month. As a result, the

differential between higher yielding 2-year bonds and 30-year bonds increased 42 basis points and approached the widest levels ever. Remarkably, the Fed’s interest rate pause provided no relief for U.S. bonds, as Treasury bond yields increased by more than Canada bond yields. Yields of 2-year and 5-year Treasuries jumped 48 and 39 basis points, respectively, while 30-year Treasury yields finished unchanged for the month. The prospect of the Fed resuming rate increases and rates staying higher for longer led to the rise in yields.

The federal sector, which is concentrated in short and mid term maturities, returned -0.30% in the month. The provincial sector, which has relatively more long term maturities, earned +0.29%. Investment grade corporate bonds returned +0.21%, as their yield spreads versus benchmark Canada bonds narrowed. The spread narrowing was particularly apparent for issues under five years to maturity as the inverted yield curve and the impact of the Bank of Canada’s rate increase provided opportunities to lock in attractive absolute yields. Non-investment grade corporate bonds earned +0.30% as their high coupon income offset some declines in their prices. Real Return Bonds earned +0.08%, thereby underperforming nominal bonds of similar duration. Preferred shares staged a partial recovery from weakness in May, earning +1.28% in June.

Since peaking in June 2022 at 8.1%, Canadian inflation has fallen quickly back to 3.4% as of May. We believe the rate is likely to decline again in the next month as the 0.7% monthly increase in June 2022 falls out of the calculation. However, after that, we expect the inflation rate to accelerate again. We note that the average monthly increase in prices in the first five months of this year has been 0.5%, far faster than the pace necessary for an annual rate of 2%. In addition, the Bank of Canada’s preferred measures of core inflation are only slightly less than 4%, indicating the fight against inflation is not nearly over. The Bank of Canada’s next two rate setting announcements are scheduled for July 12th and September 6th, and we expect the Bank will raise rates 25 basis points on one of those dates.

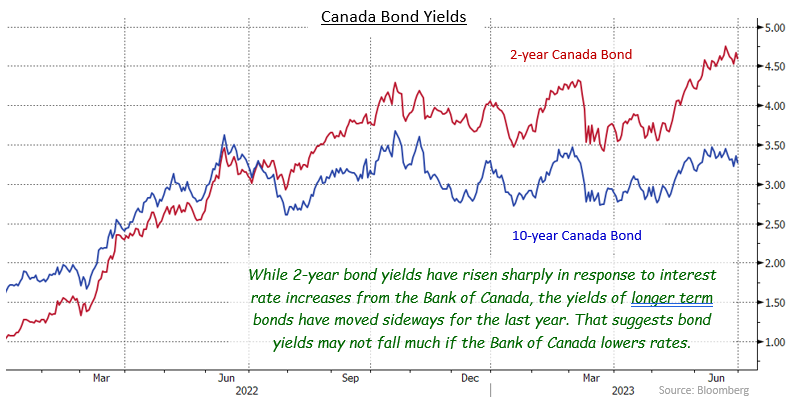

We are concerned that a recession may begin later this year or early in 2024. The resilience of the Canadian and U.S. economies to date following substantial interest rate increases shows that even tighter monetary policy is required to bring inflation sustainably down to the 2% target. That raises the likelihood of the economies reaching breaking points with sudden sharp retrenchments, rather than achieving so-called “soft landings”. The experience of the 1980’s, when inflation had become entrenched as it is currently becoming, suggests that inflation can only be curbed with a significant economic contraction that results from a substantial reduction in aggregate demand. Should a recession occur, we would expect corporate yield spreads to widen sharply in reaction to the heightened risk. Accordingly, we have reduced both the term and the absolute exposure of the corporate segment of client portfolios. A recession would also likely result in a bond market rally. We are reluctant to extend the durations of the portfolios too early because the inverted yield curve means that the portfolio yield would decline as the duration increased. We also note that the yields of longer term bonds, those with 10 years or more to maturity, have fluctuated in a range for the last twelve months, even as shorter term yields have moved substantially higher in reaction to interest rate increases from the Bank of Canada.

The lack of responsiveness of longer-term bonds to interest rates may be mirrored if and when interest rates eventually fall. Critically, Bank Governor Tiff Macklem has said that it is unlikely that interest rates will fall back to pre-pandemic levels because very low rates contributed to the surge in inflation. If the Bank eventually lowers its overnight rate to say 2.00%, fair value for 10-year bonds might not be far outside the 2.75% to 3.50% range that the bonds have traded in since June 2022.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.