Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

March 1, 2022

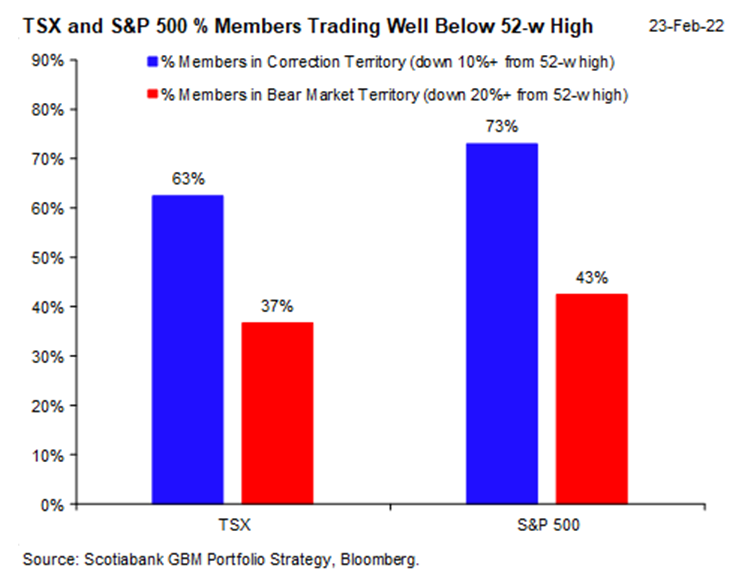

Weak stock markets so far in 2022 had been driven primarily by inflation fears and massive conjecture about the Federal Reserve and future direction of interest rates. But it took a geopolitical conflict to finally push the S&P500 into official correction territory, dropping more than 10% below its early January peak. But even before the Russia-Ukraine conflict came to the fore, most investors were already feeling the pain from the sell-off in the high growth stocks that had lead the stock market higher for most of 2020 and 2021. The 2022 decline was entirely explained by a contraction in price-earnings multiples, as 2022 earnings estimates had actually been rising, with 57% of companies and seven of eleven sectors experiencing upward revisions. But the advance was narrow, with most of the gains so far this year concentrated in the energy stocks as well as some selected cyclicals such as banks and metals. The chart below shows that 37% of stocks in the Canadian TSX and 43% of stocks in the S&P500 were already in bear markets (down more than 20%) even before the Russian armies moved into the Ukraine. The anticipation of rising interest rates to control the highest inflation rates in over 30 years had been shrinking stock valuations for the last few months, pushing the ‘tech heavy’ Nasdaq Index into an official bear market.

But stock markets always take the ‘path of least resistance’ and investors had clearly gotten positioned too bearishly following all of the worries about interest rates and then the Ukranian conflict. That is most likely why they snapped back so sharply last week after Thursday’s very weak open. This seemed more a case of “sell the rumour, buy the news” on the well-telegraphed Russian invasion of the Ukraine. Investors had gotten too bearishly positioned overall, with most high growth stocks already down more than 60% from peak levels just on the Fed rate fears as well as the inflation numbers. This was probably more of a selling exhaustion/short-covering rally, given the veracity of the rebound. There is some similarity here to 1990 when Operation Desert Shield was launched in August to take back Kuwait from the Iraqi invasion. Oil actually peaked on the day of the invasion and didn’t see those levels again for another 15 years. The difference then was that the U.S. finished up that operation in short order and markets return to normal. This time around, the conflict looks like it could take a while to get under control. The news over the past weekend about harsher sanctions imposed by the U.S and, more importantly, the EU countries make it likely that this conflict will drag on longer than anticipated. That alone could limit the upside for stocks in the short term. Add to that the continued upward pressure on inflation and Fed meeting in March where they will officially start to raise rates and may move all the way from ‘QE to ‘QT’, we think that the volatility is probably far from over. However, the lows made on Thursday morning seem to provide at least a temporary point of reprieve

Our strategy in this period of volatility has been to look for opportunities to buy stocks as earnings continue to rise and valuations have corrected sharply, particularly in the growth sectors of the market. We added late last week to some beaten up tech names (Meta, Paypal and Lightspeed) as well as some core names such as Apple, Microsoft and the semi-conductor stocks. We also bought some cyclical names such as GM, Magna, Fedex, Citi and Maxar. We lightened up on gold stocks on their sharp rally last week; while the stocks remain very cheap, gold itself is still facing short-term headwinds from a stronger US dollar. Crypto currencies failed as a ‘safe haven’ investment in the sell-off, acting more like more speculative high growth tech stocks, getting sold off on rate increase fears. It will be interesting to see if crypto currencies can pick up any of the slack being created in the global payments and savings space by the increased financial sanctions on Russian interests. We maintained our overweight in energy stocks due to their continued attractive valuation but do expect some weakening in crude oil from current levels as shortage fears subside and independent production starts to rise again, particularly in the U.S.

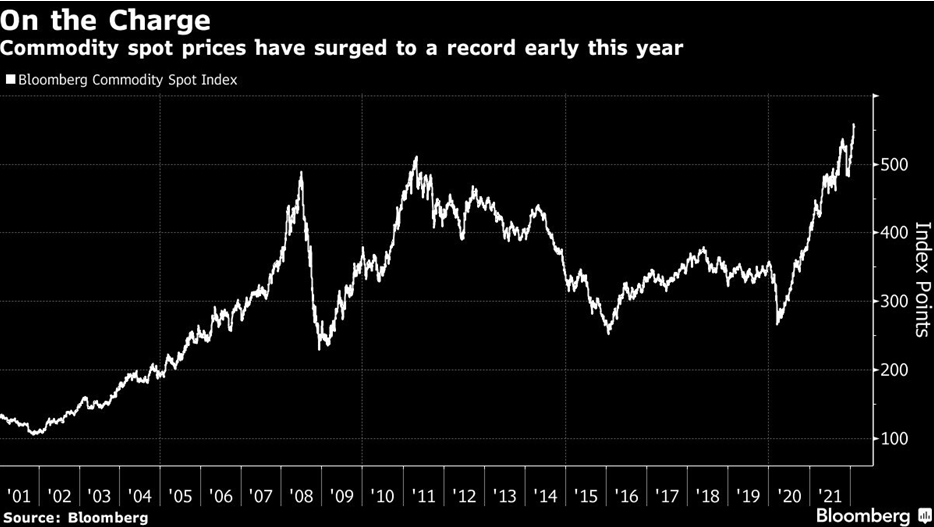

Beyond the risks from the ‘front page’ geo-political news, inflation and it’s impact on monetary policy will continue to be of greatest concern to investors. Commodity prices soared to an all-time high, underscoring the inflation concerns that prompted Fed Chairman Jerome Powell to open the door to faster rate hikes to cool the hottest price rises in almost 40 years. The Bloomberg Commodity Spot Index, which tracks 23 energy, metals and crop futures, has more than doubled from a four-year low reached early in the pandemic in March 2020. While Russia only represents about 2% of the global economy (almost identical to Canada) it represents much larger portions of key commodity markets such as oil, aluminum, fertilizers and specialty metals. Sanctions and lack of access to payments could create further supply shortages and a spike in key commodites, thus worsening an already troubling situation.

What has been most impressive about the run in commodities is that it has taken place during a period of economic instability and reduced demand as well as exceptional U.S. dollar strength, normally a headwind for commodities. The bigger catalyst for the gains has been constrained supplies, driven by rising input costs and supply chain issues. Some of those issues should get alleviated over time but there has also been a period of underinvestment in new capacity, and that is a problem that could be an overhang for the commodity sector for years. Lack of new production for copper should keep prices firm, particularly since demand continues to grow.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.