Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 31, 2020

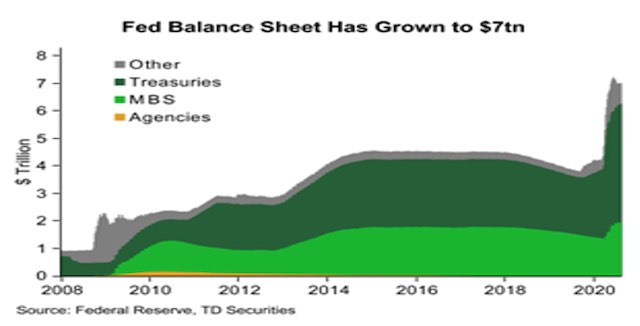

Despite ongoing economic headwinds globally from the Covid-19 pandemic, investors continued to view the future with rose-coloured glasses amidst their collective belief that the global economy will recover and, even if this takes longer than expected, central banks will continue to shower financial markets with their own massive buying of securities as well as an endless period of zero interest rates. That has been enough to fuel a stock boom larger than almost anybody would have believed back during the pandemic March lows six months ago. Since the S&P500’s nadir on March 23rd, the 50%-plus rebound marks the best 150-day gain for the big-cap benchmark on record. This has occurred despite over twenty million job losses in the U.S. alone and massive shutdowns of businesses globally. The disconnect between the stock market and underlying fundamentals seems unequivocally the greatest most of us have seen in our lifetimes. Following the shock of a mandated economic contraction, hazards melted away in ways both powerful and enduring. The huge fast fiscal-spending push and limitless central-bank money provision not only short-circuited the recession and placed a higher floor on stocks and corporate credit, it provided a real-world experiment in government authorities’ vast spending powers. In some ways the recovery is not totally illogical despite the severity of the pandemic. When we look closely at the economic numbers in the U.S., we see that the economy lost about 12% of its economic output from its peak, or about US$2.5 trillion. At the same time, the stimulus of the U.S. Federal Reserve and the additional congressional spending more than offset that decline with about US$4 trillion of stimulus. What we really saw was governments and central banks quickly ‘spending their way out’ of the downturn. This was not limited to the U.S. alone as Canada and most other industrialized countries went through similar exercises. The debt that has piled up in this rescue operation is just something that will apparently have to wait for another time to be dealt with. The chart below shows the rapid expansion in the Federal Reserve balance sheet to over US$7 trillion. Note that it was below US$1 trillion before the Financial Crisis in 2008.

The strength in the price of gold is probably mostly a reflection of this fact since the massive amounts of currency created in this rescue will only depreciate their values, thus benefitting the ‘anti-paper currency’, gold! Central bankers have spent years warning of the perils of excess corporate debt, but their solution to this year’s storm in financial markets has led to even more of it. In many ways it is the Catch-22 of post-2008 policymaking, and of now post-pandemic policymaking, too. To stave off a debt crisis, monetary policymakers create conditions that allow companies to borrow even more, increasing the potential severity of the next crisis. No central banker wants to encourage excessive borrowing but, equally, no central banker wants to stand by while companies default, increasing unemployment and throttling economic growth. The chosen solution to a debt crisis is more debt. You cannot cut it back unless you can create a tremendous amount of economic growth to offset it. The risk now is of a serious setback in the global recovery from the virus. If that happens, the additional cash borrowed by companies expecting earnings to pick back up soon may prove to be too little to see them safely through to the other side. And now, they have a whole lot more debt to grapple with. More US dollar corporate bonds have been issued so far this year than in the whole of 2019 and leverage is rising. Lenders beware, the biggest bubble may not be in stocks, but in corporate debt!

While stocks have rallied, the only trend that investors seem to have recognized is a clear distinction between the winners and losers in the new ‘work from home’ economy. Quite logically, we have seen technology stocks (particularly those involved in cloud-based businesses) as the biggest winners in the recovery and the earnings from such stalwarts as Apple, Microsoft, Salesforce, Nvidia, Amazon, Facebook and Google have justified this leadership, valuations aside for now. We have also seen home builders and home improvement retailers, online service providers and the ‘new world’ companies such as Peleton, Beyond Meat, Spotify and Netflix as big winners in this resurgence as all of those names and sectors have been beneficiaries of the transformation of the home into a ‘home office’. At the same time, investors have left behind such perennial winners as bank stocks, insurers, energy, industrials, commercial real estate, airlines and traditional ‘bricks and mortar’ retailers. As stock averages hit new daily highs they are being carried forward by fewer and fewer of the biggest names. Two years ago, there wasn’t a single company in the U.S. with a market capitalization of one trillion dollars; now there are three with Apple close to hitting two trillion. The market capitalization of the technology sector of the S&P500 now exceeds the market capitalization of the entire European stock market!

Given the sharp rise in stock prices we have to look more closely at the profit picture to see if there is any justification for the extended valuations. Corporate profits fell at an annualized rate of over 35% in the second quarter of 2020 but, given how low the ‘expectations bar’ had been set, these results proved more resilient than feared. The ‘less worse than expected’ results were both because giant, secular-growth companies such as Apple, Microsoft and Amazon account for an outsized portion of S&P500 market capitalization and because there has as yet been no painful reckoning of massive bankruptcies, since so many companies were provided emergency funds to supplements wages, pay rents and other expenses. Ample cheap credit also minimized interest payments despite record levels of corporate debt. The bottom line was that profit margins thus far have held up far better than in any prior downturns, as shown most clearly in the chart below.

Bull markets have typically been defined as ‘climbing a wall of worry.’ But along that road we eventually see optimism rise and become excessive and the bull market ends when “every last bear has been dragged, kicking and screaming, to the party.” Not sure if we’re quite there yet, but the level of infatuation on display among traders toward at least some parts of the market now seems fairly extreme and invites possible disappointment and disillusionment before too long. In bull markets strength begets strength, but only up to a point. The S&P500 is more extended further above its 200-day average than at any time in the past decade. The index’s relative strength index (RSI), a measure of momentum, recently pushed up to 80, pretty rarified air. While this is often a feature of sturdy bull markets, such readings mean no one should be surprised by a pause or sharp pullback for any reason.

The speculative buying in call options, especially on the big, beloved tech stocks, has also been voracious, driving the put/call ratio to lows not seen in a decade. The bloated prices of call options have made strong stocks more volatile as they rise, an anomaly that reflects traders and professional investors showing more optimism and aggressiveness in playing the upside than we’ve seen since the technology bubble of the late 1990s. The equity exposure level of the tactical money managers tracked by the National Association of Active Investment Managers clicked above 100, a very elevated reading suggesting performance-geared pros are roughly all-in. The risk in getting too bearish in this scenario though is the fact that this cycle has been unlike anything we’ve seen in the past so it’s probably safe to say “the old rules don’t apply.” One anomaly is that the sharpness and initial speed of the downturn in March (which saw global stock averages drop 35% within a month) and the immediacy of the overwhelming liquidity and fiscal response from the Federal Reserve and other central banks as well as most governments, forestalled the kind of grinding, purgative action of typical bear markets, which slowly wring out the excesses of the prior cycle and then reset valuations lower. There was also not the shift in market leadership that usually occurs in a bear market. Technology stocks were the leaders going into the downturn and once again assumed leadership as markets turned around, but with even greater momentum and concentration.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.