Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

February 2, 2017

While the Inauguration of President Donald Trump and his constant headline grabbing ‘executive actions’ have been the biggest drivers of the shorter-term moves in financial markets, investors are starting to get a few other items to look at that will impact stock prices. Topping that list are the fourth quarter earnings reports and initial outlooks for 2017 from many major North American companies. While the initial results from S&P500 companies have been ahead of expectations, the earnings ‘beats’ have been quite small and many were accompanied once again by ‘misses’ on the revenue lines. So once again we have companies using stocks buybacks, lower tax rates and stronger gross margins to generate earnings ahead of (lowered) expectations, but the all-important top line continues to be mediocre, at best. For U.S. export-based companies, the recent strength in the U.S. dollar has definitely created a headwind, as has the weakness in some emerging market economies. We have also seen some ‘misses’ from key growth stocks last year including Starbucks, Nike, Under Armour and UPS. Big cyclical winners have also disappointed including Caterpillar, Freeport McMoran, Exxon and Chevron. Financials have delivered earnings in line with expectations while technology results have been mixed.

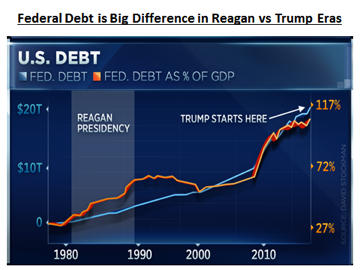

But the bigger issues for the stock market continue to come out of Washington (or Trump Tower in NYC). The early policy initiatives of the Trump Administration have been focused on manufacturing and infrastructure spending as he tries to follow through on campaign promises to increase jobs in the U.S. His agenda has given risen to comparisons to the Reagan era when the U.S. economy grew above trend, driven in large part by a substantial increase in infrastructure spending. But this is not 1980! Today the U.S. economy is coming off a period of record low interest rates versus the high double-digit rates of the early 1980’s. Moreover, stocks then were trading at earnings multiples below 10 times versus the approximate 17 times forward earnings multiple today. The big difference, though, is the level of debt! When Reagan came into the Oval Office, U.S. government debt was only 30% of GDP and the U.S. was a net global creditor. Debt today is at over 110% of GDP, a level associated with financial crises in many developed and developing economies. While Wall Street celebrated the Dow Jones Industrials Index finally crossing the 20,000 level, there is another “20” looming that could carry significantly darker overtones. The U.S. is just weeks away from passing the $20 trillion mark in total public debt outstanding — the “national debt,” as it is more widely known. Though general concern about containing debt and deficits has waned as the nation has looked for ways to stimulate the sluggish, post-recession economy, that $20 trillion milestone could grab at least some attention. Debt nearly doubled since the financial crisis in 2008, mushrooming from $10.6 to $19.9 trillion! President Donald Trump has already seen the debt rise another $2 billion.

Given these tighter financial conditions, the ability to begin to fund additional infrastructure spending without any associated tax increases would push interest rates sharply higher, an event which would undermine the ‘low interest rate valuation’ of financial markets. In the end we expect that the new administration will have to scale back some of those spending promises.

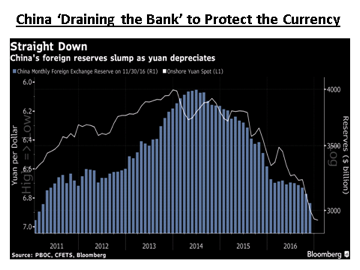

But the U.S. is not the only culprit when it comes to the accumulation of significant debt. U.S. debt levels compared to the size of their economy actually pale in comparison to what exists in China today. That country’s debt load has expanded from 150% of GDP before the onset of the 2008 global credit crisis to about 300% today. That is $30 trillion of debt sitting precariously atop a $10 trillion economy. That ratio is expected to rise further as this stimulus spending continues, on target to rise to more than 330% by next year, well above what most rating agencies view as ‘crisis levels.’ The real problem is that China has become a very ‘inefficient economy’, which is best illustrated by looking at its capital-efficiency ratio, or the number of yuan of new credit it takes to produce one yuan of GDP growth. So while China continues to borrow to sustain their growth level, the return on those borrowed dollars continues to deteriorate. China’s credit bubble now exceeds even that of the U.S. in 2007, when it was on the cusp of the subprime mortgage meltdown that set off the global credit crisis. On top of that, China has been challenged by capital outflows and declining foreign-exchange reserves. While policy makers are taking measures to solve the problem, including reducing their massive holdings of U.S. Treasury securities. China may also further sell U.S. Treasuries in 2017 if needed to keep the yuan’s exchange rate stable. China’s currency stockpile has shrunk after hitting a five-year low of $3.05 trillion in November. Capital outflows from China accelerated in recent months as the yuan suffered its worst year of losses against the U.S. dollar since 1994, declining 6.5%. About $760 billion left the country in the first 11 months of 2016, according to a Bloomberg Intelligence gauge.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.