Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

January 20, 2017

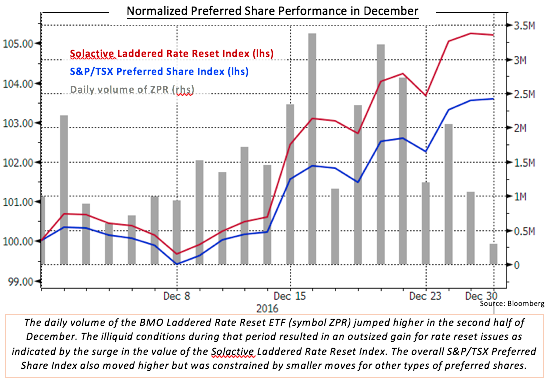

The Canadian preferred share market moved sharply higher in December as large scale buying of preferred share Exchange Traded Funds (ETFs) pushed the prices of individual issues upward. A lack of new issues contributed to the market strength. As well, in contrast with recent years, there was relatively little tax-loss selling in the December. Rate reset issues performed particularly well as a result of direct investor interest and also due to hedging of structured products. The S&P/TSX Preferred Share Index returned +3.59% in the month.

As noted above, rate reset preferred shares were especially strong, with the Solactive Laddered Rate Reset index gaining 5.21% in the month. In addition to higher than normal trading volumes, the creation of new units of the BMO Laddered Rate Reset Preferred Share Index ETF (symbol: ZPR) was particularly high, at $141 million in December, and $39 million on December 23rd alone. The recently created RBC Canadian Preferred Share ETF (symbol: RPF), which has focussed on rate reset issues, saw an additional $60 million of inflows in the month. While the RPF flows and some of the ZPR inflows reflected demand by end investors, we believe that a substantial portion of the ZPR flow was used by some banks to hedge new structured notes based on ZPR. The notes, which were both very complex and aimed at less sophisticated retail investors, have their returns linked to ZPR and became available for sale in mid-December. In some cases, the notes had principal protection, but in all cases they appeared to be expensive alternatives to index ETF’s and especially to actively managed funds.

There were no new issues of preferred shares in December. The absence of issuance was a little surprising given that issuers are sometimes opportunistic when markets are strong, but it probably reflects the relatively small number of companies that actually issue in the Canadian preferred share market. Most of the active issuers have very specific, planned capital requirements that make the issuers less responsive to market conditions.

The only rate reset shares that reset their dividend rate in December belonged to the MFC.PR.G issue. Manulife announced that insufficient numbers of the holders of those shares had wanted to convert to the floating rate alternative, so all of the holders would be receiving the new fixed rate of 3.891%, down from the original 4.40% rate.

In other corporate developments, TransAlta Corporation proposed a plan of arrangement in which all of its existing series of preferred shares would be exchanged into a single rate reset issue that would have a minimum dividend rate. TransAlta currently has four fixed rate reset series and one floating rate reset series outstanding, and all of them are trading at significant discounts to par. Under the plan, the holders of the existing preferred shares would receive a lower number of the new shares, but a higher dividend rate (6.50%) and potentially improved liquidity would compensate for this. TransAlta’s notional capital balance of outstanding preferred shares would decline by approximately $300 million, giving the company greater flexibility to issue additional preferred shares in the future. The surprise announcement resulted in some series of TransAlta preferred shares jumping 10% or more in price that day, but they remained well below par in each case. We did not hold TransAlta preferred shares because of credit concerns. The restructuring announcement did little to assuage our concerns.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.