Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

John Zechner

August 29, 2017

Stocks in the U.S. in 2017 have remained strong despite the constant flow of disruptive news coming out of Washington, ranging from the failure to enact election promises in health care, infrastructure spending and tax policy to the new tensions over the Russian investigation, elevated risk from North Korea, worsened relations with key partners such as Germany and increased polarization in the U.S., to name just a few. While most people have taken to watching far more CNN, MSNBC and FOX news over the past year, just for the ‘entertainment value’ of the White House circus, investors have chosen to look through of all of this as ‘just noise’ and to focus instead on stronger global economic growth, a reduction in regulation and an earnings recovery. We continue to question the optimism demonstrated by stock investors. While the earnings picture has gotten better this year, a large part of that is the comparisons against a very poor first half of 2016. Growth of 10% year-over-year drops to 5% when we exclude the Energy sector, which was coming off the extreme lows in 2016. Those earnings will come under pressure for the rest of 2017. Companies have also done a very good job of ‘gaming the expectations’ by setting a very low bar in terms of outlook and then surpassing those ‘lowered expectations.’

There have been some other ‘warning flags’ coming from the stock market. Overseas markets have clearly pulled back from their peaks. The heavyweight European Stoxx and German Dax Indices are each more than 5% below their recent peaks, which seems a surprise since Europe has been one of the positive surprises in terms of economic performance this year. While the U.S. market continues to be relatively strong, the gains have been accruing to a smaller and smaller group of stocks, mainly the large international technology and industrial names. There has been an alarming decline in breadth in the U.S. stock market, where return for the small-cap Russell2000 Index is now negative in 2017. Declining breadth is generally symptomatic of a stock market in its later phase. Other warning signs continue to mount for the U.S. stock market include record low volatility for an extended period of time, which tells us that investors are complacent about risk. While low volatility is rarely seen as a cause of a bear market, it has been one of the conditions in place at every market top. Throw in record stock valuations and the slow removal of low interest rate support and we continue to believe that bullish investors are ‘whistling past the graveyard’!

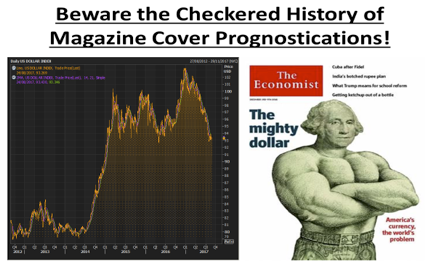

But signs of stress are showing up in areas outside of stocks. One of the most-favoured investment views going into this year was the continued strength in the U.S. dollar. The election of Donald Trump brought new optimism on growth in that economy as lower taxes, increased spending and less regulation would ‘unshackle’ growth. Moreover, the U.S. Federal Reserve had just raised interest rates again and was expected to take them higher again in 2017, making the U.S. the only economy that was removing the monetary stimulus that had been in place since the Financial Crisis. Stronger growth and higher interest rates are key ingredients for a stronger currency, so it was expected by most that the U.S. dollar would continue its upward move against the other major currencies such as the Euro and the Yen. This bullishness was featured on the cover of the December 3rd, 2016 cover of The Economist (right panel below) and referenced to by us in our January, 2017, market comments. Eight months later we are following up with the actual performance of the U.S. dollar (left panel below) and we can see that the U.S. currency basically peaked in January and has been on a steady downward path since that time, falling 10% on a trade-weighted basis.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.