Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 14, 2017

Corporate new issues totalled a record $16.9 billion in May. Interestingly, all of the issues were investment grade; there were no high yield issues in the month. Floating rate issues accounted for $2.3 billion of the funds raised, with the balance having fixed rate coupons. Maple bond issuance surged to $4.85 billion, as Pepsi, UPS, Anheuser-Busch InBev, and AT&T came to the Canadian bond market. Of the domestic issues, one of the largest was a $1.5 billion hybrid structure from TransCanada. This was the first hybrid in Canada in several years and reflected a resurgence of hybrid use in the United States. Hybrids combine features of both bonds and equities, and are based on rating agencies structuring requirements to achieve partial equity treatment. Typically, they have very long maturities, such as 50 or 60 years, but are often expected to be redeemed in only 10 years. Importantly, interest payments can be deferred by the issuer in times of financial distress, without triggering default. We did not participate in the TransCanada hybrid because of concerns about the possibility of interest deferral as well as the reliance on rating agencies to not change their rating methodology.

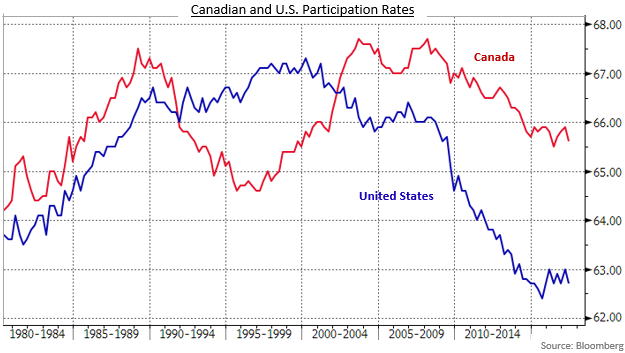

We suspect that most Canadians, if asked, would say the U.S. economy was performing better than the Canadian one. After all, the U.S. unemployment rate is 2% lower than the Canadian one, the U.S. dollar has been much stronger than the Loonie, and the Fed has been raising its interest rates while the Bank of Canada has been keeping its rates at extraordinarily low levels.

Bank of Canada has been keeping its rates at extraordinarily low levels. However, by some measures, the Canadian performance looks much more favourable. As can be seen in the chart above, Canada’s participation rate (the percentage of the working age population that is in the labour force) is well above the U.S. one, which languishes near multi-decade lows. With a larger percentage of its population economically active, Canada has greater growth potential. In addition, over the last year, Canadian GDP growth at 3.2% easily surpassed U.S. growth at 2.0%.

For bond investors, the pace of growth matters because it impacts the timing and potential for changes in monetary policy by the Bank of Canada. Recent Canadian growth has exceeded the Bank’s expectations and it has revised lower its estimates of spare capacity known as the output gap. As well, the Bank has acknowledged that the economy has finished adjusting to the impact of lower oil prices. Should Canada’s trade balance continue to improve, we believe the Bank may start raising rates in early 2018. The bond market will likely begin anticipating the Bank’s moves later this year, which should lead to somewhat lower bond prices and higher yields. The biggest impact on yields will probably be on shorter term maturities, because their yields are too close to the Bank’s current overnight target of 0.50%. The yield of 5-year Canada Bonds, at 0.95%, for example, will have little attraction for investors if the Bank begins a series of rate increases.

From a strategic perspective, we are maintaining a modestly defensive duration in the portfolios, because of the potential for yields to rise. Regarding the yield curve, we are looking to develop more of a barbell structure to protect values in the event of a flattening of the yield curve. We have been maintaining an underweight allocation to short term bonds and we will likely reduce mid-term holdings as well, in favour of increased holdings of long term bonds and cash equivalents. Given the favourable economic outlook, we continue to overweight the corporate sector, but selectivity remains very important.

Jeff Herold

Lead Fixed Income Manager

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.