Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

June 14, 2017

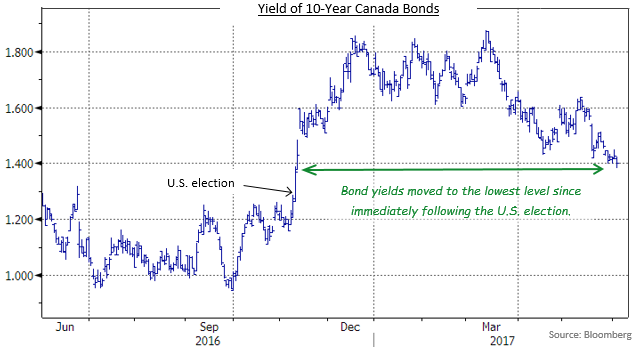

The Canadian bond market moved in seesaw fashion during May. Initially, bond prices moved lower and yields rose, but in the second half of the month prices rebounded and yields declined. By the end of the month, yields had fallen to their lowest levels since immediately following the U.S. election last November. In addition to lower yields, May was noteworthy because of record corporate bond issuance and some significant rating agency moves. The FTSE TMX Canada Universe Bond index returned 0.86% in the period.

Canadian economic data received during May was, on balance, quite favourable. Growth in Canadian GDP during the first quarter was estimated at an annual rate of +3.7%, and over the last 12 months the economy grew a robust 3.2%. Contributing to the good GDP result was an improvement in Canada’s trade balance as exports grew faster than imports. In addition, in the most recent month, the unemployment rate fell to 6.5% from 6.7%, although a sharp drop in the participation rate was the primary cause of the improvement. The Bank of Canada left its administered interest rates unchanged at its May meeting, but its accompanying statement was less dovish than expected, which caused some observers to revise their expectations of the Bank’s first rate increase to earlier in 2018.

U.S. economic data continued to show that that economy was operating at or near full capacity. The unemployment rate declined to 4.4% from 4.5% (with a lower participation rate partly responsible), and underemployment, which includes discouraged and part time workers, falling to 8.6% from 8.9%, the lowest since November 2007. Industrial production was better than expected, with broad based strength in manufacturing, utilities, and mining sectors. The data was supportive of another interest rate increase by the Federal Reserve at its June 14th meeting.

In a surprise move, the Moody’s rating agency downgraded all six of the major Canadian banks by a single rating notch in May. The increasing level of Canadian private sector debt to GDP and elevated housing prices were the primary reasons for the ratings agency’s move. The new ratings brought Moody’s assessments of credit worthiness in line with those of Standard & Poors, but below those of DBRS and Fitch. The news triggered some widening of yield spreads for bank deposit notes as well as NVCC subordinated debt. However, the modest widening followed several months of tightening yields spreads for bank debt and could be interpreted as profit taking rather than simply a reaction to the ratings change. Standard & Poors also made a notable downgrade during May. The agency lowered the Province of Alberta’s rating two notches from AA to A+, citing the province’s ongoing deficits and rising debt levels. With Alberta having a 75% economic interest in the North West Redwater refinery project, S&P also downgraded that corporate issuer. Our portfolios were not impacted by the S&P moves, because we had been avoiding Alberta bonds and we sold our North West Redwater holdings in February. On a more positive note, Moody’s upgraded Saputo (which we do own) from Baa1 to A3.

The Canadian yield curve flattened in May as longer term yields declined more than shorter term maturities; yields of 2-year Canada Bonds edged 2 basis points lower, while 30-year yields dropped 13 basis points. Lower yields at all maturities helped propel federal bond prices as the sector returned 0.67% in the month. Provincial bonds, which have longer average durations, benefitted more from the decline in long term bond yields and earned 1.35% in May. Investment grade corporate bonds lagged the government sectors, returning only 0.46% in the period. Corporate bond returns were negatively impacted by an 8 basis point widening of their yield spreads that was due to both the Moody’s downgrade of the banks and very heavy new issue supply. High yield corporate bonds earned 0.84%, while Real Return Bonds gained 1.16%. Preferred shares, which had started the year very strongly, consolidated with a -1.67% decline.

1 2

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.