Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

May 5, 2017

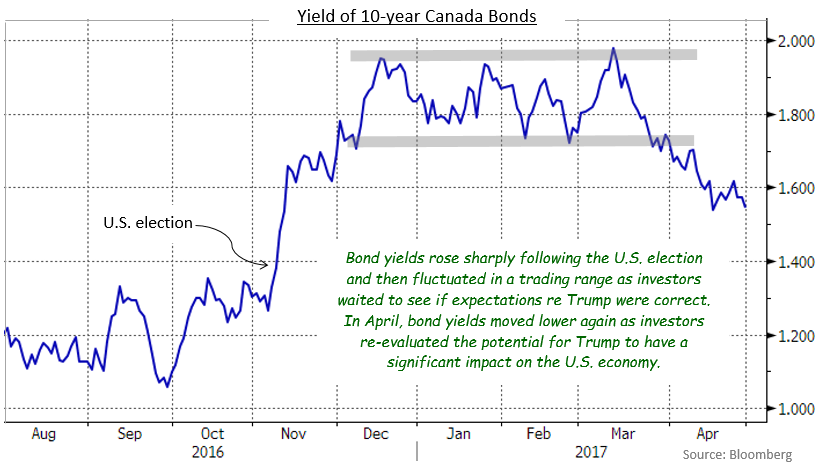

Following four months of sideways movement, bonds broke out of their trading range in April, with prices moving higher and yields declining. In large part, the catalyst for the move to lower yields appeared due to flagging optimism about the U.S. economy. The combination of weaker than expected economic data, the chaotic performance of the new Trump administration, and the inability of the U.S. Republican Party to agree on major policies such as the repeal of Obamacare caused investors to lose confidence in the anticipated economic acceleration from implementation of Trump’s election promises. Canadian bond yields followed U.S. bond yields lower. The FTSE TMX Canada Universe Bond index returned 1.43% in April.

Following a few months of relatively strong data, Canadian economic news received in April was a little softer. Canadian economic growth in the most recent month (February) was reported to have been flat, although the year-over-year growth increased to 2.5% from 2.3%. Retail sales were weaker than expected due to lower gasoline prices and reduced purchases of automobiles; other sectors experienced increased sales. Inflation was also lower than forecasts, declining to 1.6% from 2.0% the month earlier. The Bank of Canada did the expected and left interest rates unchanged, but it did acknowledge the strength of economic data in recent months and Governor Stephen Poloz said that any further rate cut was unlikely for the foreseeable future.

Sabre rattling by the U.S. government on trade matters caused the Canadian dollar to lose 2.5% against the U.S. dollar in the month. President Trump threatened to pull the United States out of the North American Free Trade Agreement as a bargaining strategy before negotiations begin on amending the treaty. In addition, the decades-old software lumber dispute resurfaced as the U.S. Commerce Department imposed tariffs on Canadian lumber following the expiration of a ten-year truce between the two countries.

In the United States, the economic news was somewhat disappointing. First quarter GDP growth was below already diminished expectations, at an annual rate of only 0.7%. Interestingly, U.S. growth in the last year was only 1.9%, notably slower than the Canadian rate. Of particular concern in the U.S. was that personal consumption increased at an annual rate of only 0.3%. Weaker than expected retail sales confirmed that consumers were reluctant to spend. New job creation was also weaker than forecasts, but the unemployment rate did fall to a cyclical low of 4.5%. The weaker data, on balance, caused U.S. bond yields to decline and prices to increase, and Canadian bonds followed suit.

The Canadian yield curve flattened in the month as the yields of 30-year bonds fell 15 basis points, while 2-year bond yields declined only 3 basis points. The existing proximity of 2-year yields, at 0.72%, to the Bank of Canada’s 0.50% overnight target, made larger declines unlikely. The biggest change in bond yields actually occurred in mid term issues, with 10-year yields moving 19 basis points lower in the month. With yields of all maturities dropping, the federal sector enjoyed good price appreciation and returned 1.00% in the month. The provincial sector, which is primarily comprised of long term bonds, gained 1.82% in the month, aided by provincial spreads narrowing 2 basis points on average. The investment grade corporate sector returned 1.53% in the month and, on a duration-neutral basis, outperformed both government sectors. Corporate yield spreads narrowed 5 basis points on average as new issue supply of $6.2 billion failed to satisfy investor demand. Non-investment grade corporates fared less well, gaining only 0.39%. Real Return Bonds, which have very long durations on average and benefitted from lower yields, returned 2.11%. Preferred shares, which had a very strong first quarter, took a breather in April, returning 0.00%.

Late in the month, the alternative mortgage lender, Home Capital Group, experienced a sudden liquidity crisis. Ontario Securities Commission allegations of misconduct by three current and former executives in 2014 and 2015 led to a run on Home Capital’s high interest savings accounts. News that the company then agreed to a usurious bailout loan from a large pension fund only reinforced the appearance of severe financial distress. However, the problems seem entirely contained to Home Capital and the impact so far on the bond market has been minimal, save for a sharp loss in value for Home Capital’s own bonds.

While we agree with the consensus that the Trump administration will have considerable difficulty delivering on election promises to raise economic growth, we believe too much credence is being given the slower economic activity in the first three months of the year. Weakness of U.S. economic data in the first quarter of a year is hardly a new phenomenon; initial reports on first quarter GDP growth have been much lower than economists’ forecasts in each of the last 8 years. Perhaps wonky seasonal adjustment factors are to blame but, in most cases, growth has rebounded over the balance of the year. We suspect that the pattern will repeat itself in 2017. Accordingly, we are being patient regarding portfolio durations, preferring to remain slightly shorter than benchmarks.

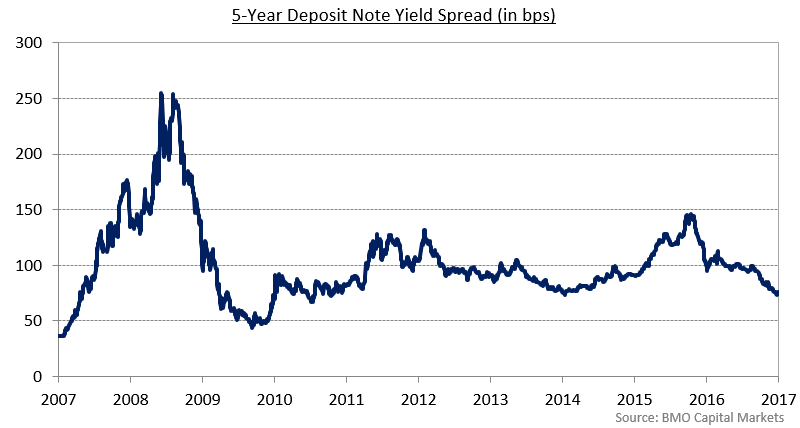

For some time, the corporate sector has been our preferred one because the yield spreads have been attractive. As those spreads have compressed, corporate bonds enjoyed price gains relative to their underlying Canada benchmark bonds. However, the narrowing of corporate spreads over the last several months has brought them to the tightest levels since the financial crisis. At this point, corporate bonds appear fairly valued, but are no longer “cheap” in our opinion. As can be seen in the following chart,

deposit note yield spreads have been narrower on occasion in the past, but relatively infrequently. The same is true for the spreads of other types of corporate issues such as long term utility bonds. Less potential for yield spreads to narrow reduces the likelihood of enhanced returns due to capital gains, so we are evaluating whether to reduce the allocation to the corporate sector.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.