Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

July 31, 2017

While the commodity rally of 2016 was driven by the U.S dollar depreciation, we believe the commodity rally we will experience in the back half of 2017, will be demand driven. We remain considerably over weight the base metal sector to take advantage of this scenario. With respect to gold, current inflation indicators are benign, however most central banks (led by the US Fed) continually warn that inflation is set to push higher over the next 6 – 12 months. While we expect gold prices to stay within a tight range over the next quarter, we continue to find many opportunities for investments in the smaller gold companies, where money is being put to work to find ounces. The majors continue to face a production cliff and we believe the M & A cycle will begin to heat up. Seasonally, we are also entering a typically strong period for gold equities. As such, we continue to hold overweight positions in the precious metal sector, focusing on growth names which focus on exploration and ramping up production. These company’s stock prices should be less correlated to the price of gold and more connected to company and project milestones.

The second quarter punished the gold sector, a major index rebalancing (the GDXJ ETF) had a very negative impact on the funds flow within the small cap gold names. This resulted in a sizable check back in the sector, that was not based on fundamentals and valuations. We believe this put unwarranted pressure on many of the gold stocks in the portfolio and has created a good opportunity for long term investors.

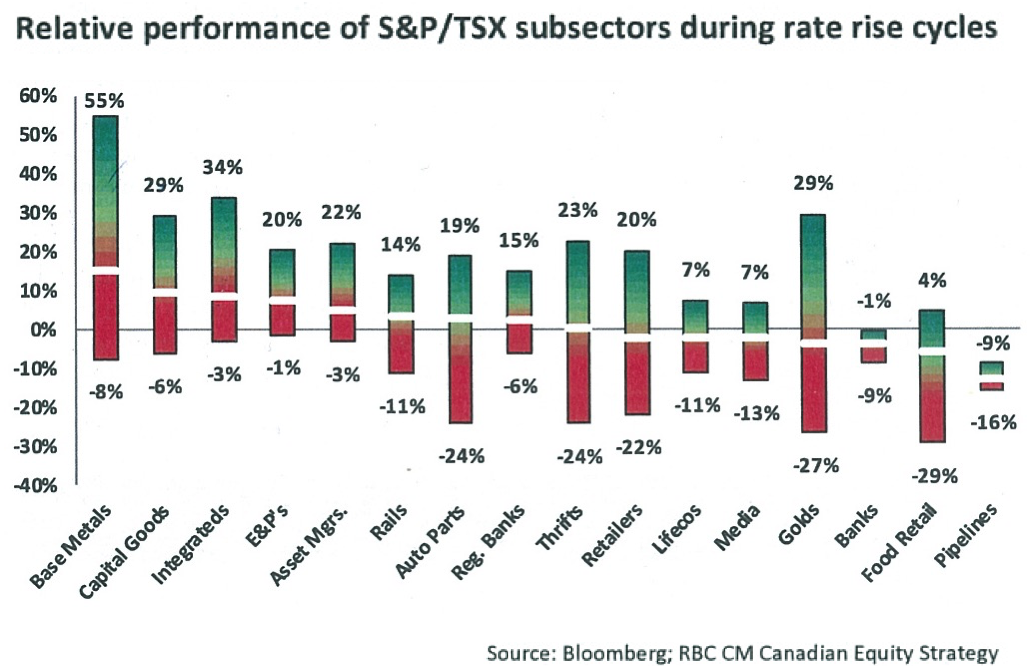

Given the global back drop of rising rates, we have included some interesting charts from a report RBC did on the impact of rising rates on various sectors and sub sectors of the S&P / TSX. As is evident from the chart, late stage cyclicals tend to outperform more defensive sectors such as Banks, Retailers and Utilities. The portfolio continues to hold an overweight position in the late cyclicals and special growth situations.

Challenges within the resource market in the first half of 2017 are reflected in the portfolio returns. Year to date the portfolio has underperformed the S&P TSX small cap index by -5.1%. The under performance came largely in the 2Q with largest losses in June. Yangarra Resources, Tecsys Inc. and Shopify Inc were the three best performing stocks in the quarter, adding 1.52% to overall returns. The three worst performing names were Asanko Gold, Dealnet Capital Corp. and Leucrotta Exploration Inc. These three names detracted – 1.65% last quarter.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.