Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

July 12, 2017

Global bond markets were weak in June, as central banks worldwide shifted to a more hawkish stance. With economic growth improving in most advanced economies, the need for quantitative easing and ultra-low interest rates diminished and central bankers started planning for gradual reductions in stimulus. The Canadian bond market was one of the weakest in the world during June as the Bank of Canada made a more abrupt change in its policy. After two years of defending its 2015 rate reductions and deflecting blame for the resultant housing bubble in Vancouver and Toronto, the Bank suggested the rate cuts had had the desired effect and interest rate increases could now be anticipated. Bond prices fell as yields rose in anticipation of higher interest rates. The FTSE TMX Canada Universe Bond index returned -1.17% in June. So far this year, the index has earned +2.36%.

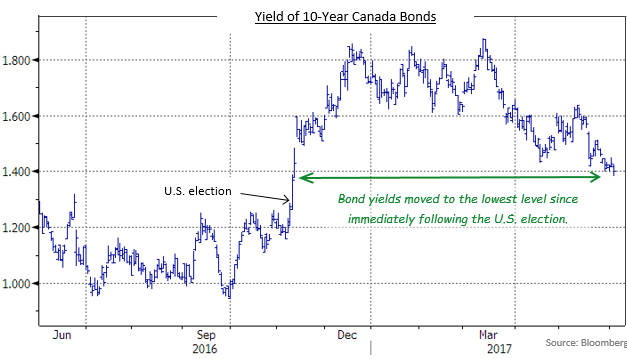

On June 12th, the Bank of Canada’s Senior Deputy Governor, Carolyn Wilkins, gave a speech that strongly hinted the Bank was considering raising interest rates. She said the economy no longer required the current extraordinary stimulus. Subsequent statements by the Bank’s Governor and other officials reinforced Wilkins’s message. Bond yields, particularly for shorter maturities, moved sharply higher over the balance of the month as investors discounted the possibility of a rate increase as soon as the Bank’s July 12th meeting.

Trying to understand and anticipate the Bank of Canada monetary policy moves these days is reminiscent of Winston Churchill’s description of Russia as “a riddle, wrapped in a mystery, inside an enigma”. For example, the surprise rate reduction in January 2015 (followed by a second cut in July of that year) was ostensibly to offset the impact of the precipitous drop in the price of oil. However, lower borrowing costs were not likely to have much impact on the earnings or the investment plans of energy companies dealing with oil at $26 per barrel. When we have asked various Deputy Governors to illustrate the effectiveness of the two rate reductions in 2015, they have responded with the unproveable “It would have been worse if we had done nothing.” More recently, the timing of Wilkins’s announcement was almost random given the strength in Canada’s economy over the last few quarters. With Canada having the best economic growth rate in the G7 over the last year, the Bank could have justified rate increases months ago, so the question is not why, but why now? We don’t have an answer, and judging by the market reaction, neither does anyone else.

The Canadian economy continued to perform well as evidenced by data received in June. Canada’s GDP increased 3.3% in the most recent 12 months, the fastest pace of any of the major industrialized countries. Job creation was quite strong, although the unemployment rate held steady at 6.6%, because the participation rate rebounded from a weak reading the previous month. In addition, retail and wholesale sales were stronger than expected. Inflation was one of the few areas of concern as CPI slowed to 1.3% from 1.6%, but the slowdown was thought the result of temporary factors such as the Ontario electricity rebate.<--!nextpage-->

In the United States, the economic data was somewhat disappointing. Retail sales, housing starts, and vehicle sales were each weaker than expected. Job creation was slower than forecasts, although the unemployment rate dipped to 4.3% from 4.4% because the participation rate declined. As in Canada, the inflation rate dropped (to 1.9% from 2.2%) but the decrease was thought to be due to temporary factors. Notwithstanding the slower economic indicators, the U.S. Federal Reserve implemented its third consecutive quarterly rate increase of 0.25% in June. The Fed also outlined its plan to reduce its balance sheet by gradually reducing the number of bonds and mortgage-backed securities that it would hold. No date was given for the balance sheet reduction plan to start, but many observers expect that it will begin this year. Over the next several years, the Fed will likely shed approximately $2 trillion of securities, which will put upward pressure on yields no matter what the pace.

Internationally, the Bank of England left its administered interest rates unchanged, but 3 of the 8 voters wanted to raise them. The Bank’s Governor, Mark Carney, voted against a rate increase, but subsequently appeared more open to the possible move. However, any U.K. increase may be delayed because of the Brexit negotiations. In Europe, the President of the European Central Bank, Mario Draghi, noted the improvement in both economic growth and inflation, but suggested any reduction in the ECB’s monetary stimulus would be very gradual. Currently, its quantitative easing programme is scheduled to run until December, with little likelihood of an earlier finish.

The Canadian yield curve flattened significantly as the yields of shorter term bonds spiked higher in anticipation of rate increases by the Bank of Canada. The yields on 2 and 5-year Canada Bonds rose 40 and 42 basis points, respectively, to the highest levels since prior to the Bank’s first surprise rate reduction in January 2015. The increases in 10 and 30-year yields were more muted at 33 and 8 basis points, respectively. The yields of longer term issues only retraced portions of the declines experienced earlier this year and failed to establish new highs. The shift in the Canadian yield curve was much more dramatic than the U.S., where 2-year Treasury yields rose 11 basis points and 30-year yields actually declined 2 basis points.

The federal sector returned -1.45% in June, as the substantial increase in yields during the month resulted in sharp declines in bond prices. The provincial sector fared better, notwithstanding its longer average duration, and returned -1.04%. The smaller yield moves of longer maturities resulted in smaller price drops for provincial issues. As well, provincial yield spreads narrowed by 5 basis points, on average. The corporate sector returned -0.96% in the period, helped by yield spreads narrowing 5 basis points. The tighter corporate spreads represented a partial recovery from May’s widening and were the result of new issuance falling from record levels a month ago. New issues in June totalled $12.6 billion, of which $9.6 billion were fixed rate bonds and the balance were floating rate notes. Also in the period, non-investment grade corporate bonds earned +0.46%, as investors continued to stretch for higher yields. Real Return Bonds declined -1.87% in the month, as they were impacted by both higher nominal yields and weaker inflation. Following lacklustre results in the previous two months, preferred shares bounced back strongly, earning +2.84% in the month. <--!nextpage-->

Considering the Bank of Canada’s hints during June, it seems highly likely that it will raise interest rates by 0.25% at its July 12th meeting. There seems little reason for the Bank in June to start preparing the market for a rate increase in the fall, so we believe its intention was to move sooner. Another rate increase in the fall would fully reverse the Bank’s 2015 rate cuts and we expect that the Bank will then pause to evaluate the impact of the rate increases and to avoid catching up to the Fed’s 1.25% target rate. We think the Fed will skip raising rates again at its September meeting, and choose to start reducing its balance sheet instead.

The adjustment in yields following the Bank of Canada’s policy stance has made short and mid term bonds more reasonably priced. The yield of 5-year Canada Bonds, for example, has risen close to 1.50%, which appears to fully discount for the two rate increases that are expected over the balance of 2017. Accordingly, we anticipate reversing some of the yield flattening trades made in June. As part of this, cash levels should be reduced from their current, elevated levels.

As we noted a couple of months ago, corporate bonds appear fairly valued, but are no longer cheap. Selectivity remains key, and we are considering reductions in the corporate sector allocation. We are also looking at the relative spreads for corporate issuers at different terms. If there is little difference in risk premiums between different maturities, it may make sense to reduce terms.

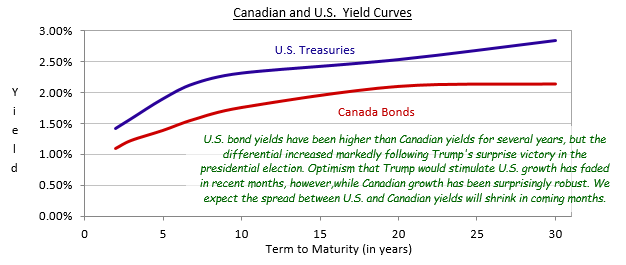

We remain somewhat defensive regarding duration for two reasons. First, the trend globally appears to be toward higher yields, as central banks remove or prepare to remove some of the extraordinary monetary stimulus that has been in place. Second, Canadian bonds appear expensive compared to those of the United States. The differential between the two countries’ bonds widened following Donald Trump’s election, but as the U.S. administration flounders it seems likely that the yield spreads will narrow. The better relative economic performance of Canada also argues for Canadian yields to move closer to their American counterparts

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.