Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jacqueline Ricci

In the first quarter of 2020, global markets around the world were hijacked by the coronavirus. As economies, one by one, began shutting down to stem the pandemic, the global outlook for corporate earnings and economic growth were decimated. The pandemic, unprecedented in our lifetime, caused markets to fall at a precipitous rate, with the SPTSX dropping -37% in 31 days. Not surprising the small capitalization stocks were severely hit.

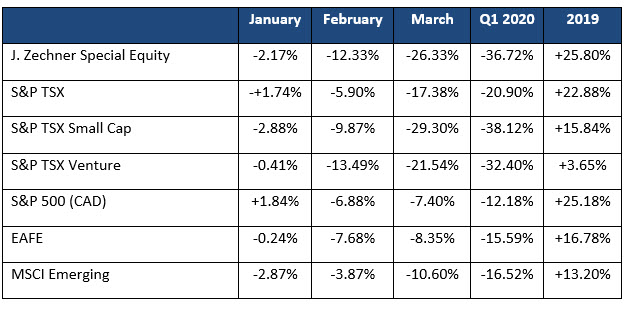

Below is a table of the portfolio and global equity market returns.

Of note, the portfolio was able to relatively outperform the SPTSX Small Cap index, losing -36.7% for the quarter. Historically the portfolio does have a higher beta than the market so it may be somewhat surprising that there was a relative outperformance given the significant decline. The outperformance is attributable to some of the actions we took earlier in the year which included taking our overweight in the energy sector to an underweight and increasing the portfolio’s gold weight. The portfolio historically is underweight the consumer discretionary sector and this was a sector that was hit particularly hard in the sell-off.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.